Examinable Auditing Standards for December 2015 and June 2016 Sessions

- 格式:pdf

- 大小:77.11 KB

- 文档页数:3

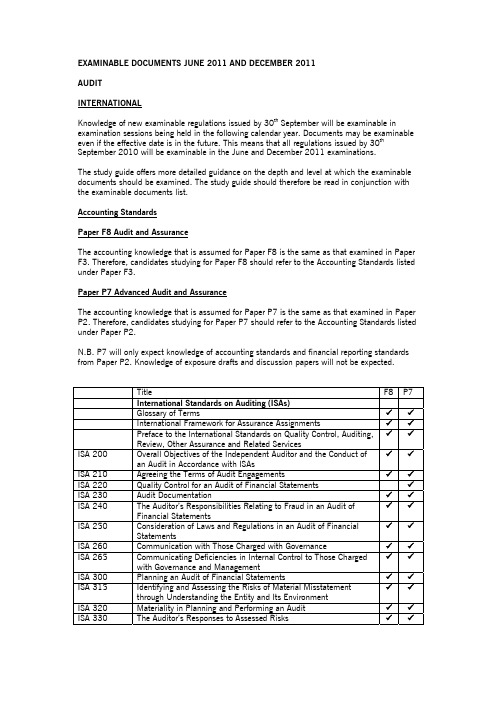

EXAMINABLE DOCUMENTS JUNE 2011 AND DECEMBER 2011AUDITINTERNATIONALKnowledge of new examinable regulations issued by 30th September will be examinable inexamination sessions being held in the following calendar year. Documents may be examinableeven if the effective date is in the future. This means that all regulations issued by 30thSeptember 2010 will be examinable in the June and December 2011 examinations.The study guide offers more detailed guidance on the depth and level at which the examinabledocuments should be examined. The study guide should therefore be read in conjunction withthe examinable documents list.Accounting StandardsPaper F8 Audit and AssuranceThe accounting knowledge that is assumed for Paper F8 is the same as that examined in PaperF3. Therefore, candidates studying for Paper F8 should refer to the Accounting Standards listedunder Paper F3.Paper P7 Advanced Audit and AssuranceThe accounting knowledge that is assumed for Paper P7 is the same as that examined in PaperP2. Therefore, candidates studying for Paper P7 should refer to the Accounting Standards listedunder Paper P2.N.B. P7 will only expect knowledge of accounting standards and financial reporting standardsfrom Paper P2. Knowledge of exposure drafts and discussion papers will not be expected.P7 Title F8 International Standards on Auditing (ISAs)Glossary of Terms 99for Assurance Assignments 99FrameworkInternational99Preface to the International Standards on Quality Control, Auditing,Review, Other Assurance and Related Services99ISA 200 Overall Objectives of the Independent Auditor and the Conduct ofan Audit in Accordance with ISAsISA 210 Agreeing the Terms of Audit Engagements 99ISA 220 Quality Control for an Audit of Financial Statements 9ISA 230 Audit Documentation 9999ISA 240 The Auditor’s Responsibilities Relating to Fraud in an Audit ofFinancial Statements99ISA 250 Consideration of Laws and Regulations in an Audit of FinancialStatementsISA 260 Communication with Those Charged with Governance 9999ISA 265 Communicating Deficiencies in Internal Control to Those Chargedwith Governance and ManagementISA 300 Planning an Audit of Financial Statements 9999ISA 315 Identifying and Assessing the Risks of Material Misstatementthrough Understanding the Entity and Its EnvironmentISA 320 Materiality in Planning and Performing an Audit 99ISA 330 The Auditor’s Responses to Assessed Risks 9999 ISA 402 Audit Considerations Relating to an Entity Using a ServiceOrganisationISA 450 Evaluation of Misstatements Identified During the Audit 99 ISA 500 Audit Evidence 99 ISA 501 Audit Evidence – Specific Considerations for Selected Items 99 ISA 505 External Confirmations 99 ISA 510 Initial Audit Engagements – Opening Balances 99 ISA 520 Analytical Procedures 99 ISA 530 Audit Sampling 9999 ISA 540 Auditing Accounting Estimates, Including Fair Value AccountingEstimates and Related DisclosuresISA 550 Related Parties 9 ISA 560 Subsequent Events 99 ISA 570 Going Concern 99 ISA 580 Written Representations 999 ISA 600 Special Considerations - Audits of Group Financial Statements(Including the Work of Component Auditors)ISA 610 Using the Work of Internal Auditors 99 ISA 620 Using the Work of an Auditor’s Expert 99 ISA 700 Forming an Opinion and Reporting on Financial Statements 99 ISA 705 Modifications to the Opinion in the Independent Auditor’s Report 9999 ISA 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs inthe Independent Auditor’s Report99 ISA 710 Comparative Information – Corresponding Figures and ComparativeFinancial Statements99 ISA 720 The Auditor’s Responsibilities Relating to Other Information inDocuments Containing Audited Financial StatementsInternational Auditing Practice Statements (IAPSs)IAPS 1000 Inter-bank Confirmation Procedures 99 IAPS 1010 The Consideration of Environmental Matters in the Audit ofFinancial StatementsIAPS 1013 Electronic Commerce: Effect on the Audit of Financial Statements 99 International Standards on Assurance Engagements (ISAEs)99 ISAE 3000 Assurance Engagements other than Audits or Reviews of HistoricalFinancial InformationISAE 3400 The Examination of Prospective Financial Information 9 ISAE 3402 Assurance Reports on Controls at a Service Organisation 9 International Standards on Quality Control (ISQCs)9 ISQC 1 Quality Controls for Firms that Perform Audits and Reviews ofFinancial Statements, and Other Assurance and Related ServicesEngagementsInternational Standards on Related Services (ISRSs)9 ISR 4400 Engagements to Perform Agreed-Upon Procedures RegardingFinancial InformationInternational Standards on Review Engagements (ISREs)ISRE 2400 Engagements to Review Financial Statements 99 ISRE 2410 Review of Interim Financial Information Performed by theIndependent Auditor of the EntityExposure Drafts (EDs)Auditing Complex Financial Statements 99 Proposed ISA 315 (Revised) Identifying and Assessing the Risks ofMaterial Misstatement through Understanding the Entity and ItsEnvironmentProposed ISA 610 (Revised) Using the Work of Internal Auditors 9Other DocumentsACCA’s ‘Code of Ethics and Conduct’ 999 IFAC’s ‘Code of Ethics for Professional Accountants’ (Revised July2009)9 ACCA’s Technical Factsheet 94 – Anti Money-Laundering(Proceeds of Crime and Terrorism)9 The UK Corporate Governance Code as an example of a code ofbest practice9 The UK Corporate Governance Code as an example of a code ofbest practice in relation to audit committess9 IAASB Practice Alert Challenges in Auditing Fair Value AccountingEstimates in the Current Market Environment (October 2008)9 IAASB Practice Alert Audit Considerations in Respect of GoingConcern in the Current Economic Environment (January 2009)9 IAASB Applying ISAs Proportionately with the Size and Complexityof an Entity (August 2009)9 IAASB Practice Alert Emerging Practice Issues Regarding the Useof External Confirmations in an Audit of Financial Statements(November 2009)IAASB XBRL : The Emerging Landscape (January 2010) 99 IAASB Auditor Considerations Regarding Significant Unusual orHighly Complex Transactions (September 2010)Note:Topics of exposure drafts are examinable to the extent that relevant articles about them are published in student accountant.EXAMINABLE DOCUMENTS JUNE AND DECEMBER 2011AUDITUKKnowledge of new examinable regulations issued by 30th September will be examinable inexamination sessions being held in the following calendar year. Documents may be examinableeven if the effective date is in the future. This means that all regulations issued by 30thSeptember 2010 will be examinable in the June and December 2011 examinations.The study guide offers more detailed guidance on the depth and level at which the examinable documents should be examined. The study guide should therefore be read in conjunction withthe examinable documents list.Accounting StandardsAll questions set will be based on International Financial Reporting Standards.Paper F8 Audit and AssuranceThe accounting knowledge that is assumed for Paper F8 is the same as that examined in PaperF3. Therefore, candidates studying for Paper F8 should refer to the Accounting Standards listedunder Paper F3.Paper P7 Advanced Audit and AssuranceThe accounting knowledge that is assumed for Paper P7 is the same as that examined in PaperP2. Therefore, candidates studying for Paper P7 should refer to the Accounting Standards listedunder Paper P2.N.B. P7 will only expect knowledge of accounting standards and financial reporting standardsfrom Paper P2. Knowledge of exposure drafts and discussion papers will not be expected.Title F8P7 International Standards on Auditing (ISAs) (UK and Ireland)Summary of changes to the new ISAs (UK and Ireland) 9Glossary of terms 2009 9999ISA 200 Overall objectives of the independent auditor and the conduct of anaudit in accordance with ISAs (UK and Ireland)ISA 210 Agreeing the terms of audit engagements 99ISA 220 Quality control for an audit of financial statements 9ISA 230 Audit documentation 9999ISA 240 The Auditor’s responsibilities relating to fraud in an audit of financialstatements99ISA 250A Consideration of laws and regulations in an audit of financialstatementsISA 260 Communication with those charged with governance 9999ISA 265 Communicating deficiencies in internal control to those charged withgovernance and managementISA 300 Planning an audit of financial statements 9999ISA 315 Identifying and assessing the risks of material misstatement throughunderstanding the entity and Its environmentISA 320 Materiality in planning and performing an audit 99ISA 330 The auditor’s responses to assessed risks 99Title F8P7ISA 402 Audit considerations relating to entities using a service organisation 99ISA 450 Evaluation of misstatements identified during the audit 99ISA 500 Audit evidence 99ISA 501 Audit evidence – specific considerations for selected items 99ISA 505 External confirmations 99ISA 510 Initial audit engagements – opening balances 99ISA 520 Analytical procedures 99ISA 530 Audit sampling 9999ISA 540 Auditing accounting estimates, including fair value accountingestimates and related disclosuresISA 550 Related parties 9ISA 560 Subsequent events 99ISA 570 Going concern 99ISA 580 Written representations 999ISA 600 Special considerations - audits of group financial statements (includingthe work of component auditors)ISA 610 Using the work of internal auditors 99ISA 620 Using the work of an auditor’s expert 99ISA 700 The auditor’s report on financial statements 99ISA 705 Modifications to opinions in the independent auditor’s report 9999ISA 706 Emphasis of matter paragraphs and other matter paragraphs in theindependent auditor’s report99ISA 710 Comparative information – corresponding figures and comparativefinancial statements99ISA 720A The auditor’s responsibilities relating to other information in documentscontaining audited financial statements99ISA 720B The auditor’s statutory reporting responsibility in relation to directors’reportsInternational Standards on Quality Control (ISQC)9ISQC 1 Quality control for firms that perform audits and reviews of financialstatements and other assurance and related services engagementsPractice Notes (PNs)9PN 12 (Revised) Money Laundering – Guidance for auditors on UK legislation(September 2010)PN 16 Bank reports for audit purposes in the United Kingdom (Revised) 999PN 23 (Revised) Auditing complex financial instruments – interim guidance(October 2009)PN 25 Attendance at stocktaking 9999PN 26 (Revised) Guidance for smaller entity audit documentation (December2009)Ethical Standards (ESs)ES (Revised – April 2008) Provisions available for small entities 99ES1 (Revised – April 2008) Integrity, objectivity and independence 9999ES2 (Revised - April 2008) Financial, business, employment and personalrelationshipsES3 (Revised – October 2009) Long association with the audit engagement 9999ES4 (Revised – April 2008) Fees, remuneration and evaluation policies,litigation, gifts and hospitalityES5 (Revised – April 2008) Non-audit services provided to audit clients 99Glossary 99 Bulletins2001/03 E-business: identifying financial statement risks 9992008/01 Audit issues when financial market conditions are difficult and creditfacilities may be restrictedP7 Title F82008/06 The ‘senior statutory auditor’ under the United Kingdom CompaniesAct 200692008/10 Going Concern Issues During the Current Economic Conditions 99 2009/2 Auditor’s Reports on Financial Statements in the United Kingdom 99 2009/4 Developments in corporate governance affecting the responsibilities ofauditors of UK companies92010/1 XBRL tagging of information in audited financial statements – guidance for auditors9 Statement of Standards for Reporting Accountants (SSRAs)ISRE (UK and Ireland) 2410 Review of Interim Financial Information Performed by the IndependentAuditor of the Entity9Exposure Drafts (EDs) (UK and Ireland)Consultation Paper : Revised Draft Ethical Standard for Auditors 9 Consultation Draft : Practice Note 25 Attendance at Stocktaking(Revised)Consultation Draft : Practice Note 16 Bank reports for audit purposesin the United Kingdom9Discussion Paper Auditor Scepticism : Raising the Bar 9 Consultation Draft : ISA (UK and Ireland) 700 The auditor’s report onfinancial statements9The Provision of Non-Audit Services by Auditors Consultation Paper on Revised Draft Ethical Standards for Auditors9Other DocumentsACCA’s ‘Code of Ethics and Conduct’ 99 IFAC’s ‘Code of Ethics for Professional Accountants’ (Revised July2009)9The UK Corporate Governance Code 9The UK Corporate Governance Code in relation to audit committees 9 Going Concern and Liquidity Risk : Guidance for Directors of UKCompanies 20099Scope and Authority of APB Pronouncements (Revised) – October200999ACCA’s Technical Factsheet 94 – Anti-Money Laundering (Proceeds ofCrime and Terrorism)9IAASB Practice Alert Challenges in Auditing Fair Value AccountingEstimates in the Current Market Environment (October 2008)9IAASB Applying ISAs Proportionately with the Size and Complexity ofan Entity (August 2009)9IAASB Practice Alert Emerging Practice Issues Regarding the Use ofExternal Confirmations in an Audit of Financial Statements (November2009)9IAASB Auditor Considerations Regarding Significant Unusual or Highly Complex Transactions (September 2010)9Note:Topics of exposure drafts are examinable to the extent that relevant articles about them are published in student accountant.。

中国注册会计师审计准则应用指南英语全文共6篇示例,供读者参考篇1The Very Important Guide for Checking NumbersHi there, kids! Today we're going to learn about a super important book called the Chinese Certified Public Accountant Auditing Standards Application Guide. That's a really long name, so let's just call it "The Number Checker's Guide" for short.This guide is like a rule book that grown-ups called auditors use when they need to check that businesses are keeping track of their money correctly. Just like you have to follow the rules in school, businesses have to follow the rules in this book when they count their dollars and cents.The Number Checker's Guide has loads of different rules and instructions. It tells the auditors exactly how they should look over all the numbers to make sure nothing is missing or wrong. That way, we can trust that the businesses are being honest about their money.Let me give you an example of how it works. Let's say you have a lemonade stand and you sell lemonade for 25 cents a cup. The Number Checker's Guide would tell the auditors how to make sure you counted up your quarters correctly at the end of the day.First, they would check that you wrote down every sale in a logbook, just like the guide says. Then they would count all the quarters in your money box and make sure the total matches the number of lemonade cups you sold according to your logbook.If the numbers don't match up, then the auditors know that there was a mistake somewhere. Either you forgot to log some sales, or maybe you miscounted your quarters. The Number Checker's Guide helps them figure out what went wrong.But it's not just about lemonade money! The Number Checker's Guide has rules for checking all kinds of numbers that businesses deal with. Like if a company orders supplies or builds a new factory, the auditors check that the costs were all recorded properly following the rules.The guide also gives instructions on how auditors should behave when they go check a business. It tells them to be honest, independent, and never take bribes or do anything shady. That'sreally important, because we need to be able to trust that the auditors aren't helping businesses cheat on their math!There are tons of different rules about all sorts of stuff like keeping documents safe, interviewing employees, checking computer programs, and more. The Number Checker's Guide is like an encyclopedia of auditing!Auditors have to study this guide really hard to learn all the rules. It's kind of like how you have to study really hard for your math tests, except their tests are way harder! After they learn it all, they can call themselves Certified Public Accountants. That's a fancy way to say they are number checking experts who follow the rules in the guide.So next time your family goes to a restaurant or buys something from a store, you can thank the auditors who use the Number Checker's Guide. Because of their hard work, we know that businesses aren't fibbing about their money. Pretty cool, huh?Learning how to check numbers properly is super important as you start to grow up. Who knows, maybe someday you'll want to get a cool job as an auditor too! But for now, you can practice by carefully counting your pennies and making sure you always follow the rules, just like the Number Checker's Guide says.篇2Title: A Fun Guide to Auditing for Kids!Hey there, kids! Have you ever wondered what auditing is all about? Well, get ready for an exciting adventure into the world of numbers and rules!Auditing is like playing detective, but instead of solving mysteries, we make sure that companies are following the right accounting rules. Think of it as a game where you have to check if everything adds up correctly.In China, we have a special set of rules called the Chinese Certified Public Accountant Auditing Standards Application Guide. These rules are like the instruction manual for auditors, telling them exactly what to do when checking a company's books.Now, let's imagine you're an auditor working for a big accounting firm. Your job is to make sure that a company's financial statements are accurate and follow all the rules. It's like being a superhero, but instead of fighting bad guys, you're fighting against mistakes and errors!First, you need to plan your audit mission. You'll decide which areas of the company you want to focus on and gather all the information you need. It's like getting your spy gear ready before going on a secret mission!Next, you'll have to assess the risks involved. Are there any areas where mistakes are more likely to happen? It's like looking for clues to find out where the trouble spots might be.Once you've identified the risks, it's time to gather evidence. You'll request documents, interview employees, and observe how the company operates. It's like collecting clues at a crime scene, but instead of fingerprints, you're looking for numbers that don't add up.As you gather evidence, you'll need to keep detailed records of everything you find. This is called documentation, and it's like keeping a secret diary of all your adventures.If you discover any errors or problems, you'll have to report them to the company. This is called issuing an audit opinion, and it's like giving the company a report card on how well they've followed the rules.But wait, there's more! After you've completed your audit, you'll need to communicate your findings to the company'smanagement and those in charge of governance. It's like having a big meeting to discuss your secret mission and how it went.Throughout the entire process, you'll need to follow the Chinese Certified Public Accountant Auditing Standards Application Guide. These rules are like your trusty guidebook, helping you navigate through the world of auditing and making sure you do everything correctly.Auditing may sound complicated, but it's really just a game of following the rules and making sure companies are playing fair. And who knows, maybe one day you'll become a superhero auditor, fighting against financial crimes and keeping the world of accounting safe!So, what do you say, kids? Are you ready to join the exciting world of auditing? Remember, with the Chinese Certified Public Accountant Auditing Standards Application Guide by your side, you'll be unstoppable!篇3The Super Important Auditing Guide for Certified AccountantsHi there, kids! Today we're going to learn about a very important book called the Chinese Certified Public Accountants Auditing Standards Application Guide. It might sound like a mouthful, but it's a crucial set of rules that accountants need to follow when they check the books and finances of companies and organizations. Think of it as a playbook that helps accountants do their jobs properly!You know how your teachers have rules in the classroom that everyone needs to obey? Well, this guide is like that, but for accountants who work with numbers and money all day. Just like you have to raise your hand before speaking in class, accountants have to follow certain steps and guidelines when they audit (that means check) a company's financial records.Now, let's imagine you're a detective, and your job is to make sure nobody is cheating or breaking any rules when it comes to money. That's kind of what auditors (accountants who do audits) do. They look at a company's books, receipts, bank statements, and other financial documents to make sure everything adds up correctly and that no one is cooking the books (which means falsifying or changing the numbers illegally).The Auditing Standards Application Guide is like a detective's handbook that tells auditors exactly what they need to do to solve the case and catch any financial wrongdoings. It covers all sorts of important topics, like how to plan an audit, what kind of evidence they need to collect, how to test different areas of a company's finances, and how to write up their final report with their findings.One of the key things this guide emphasizes is something called "professional skepticism." That means auditors can't just take a company's word for it when they say their finances are all in order. Auditors have to be like detectives who question everything and look for any clues or red flags that something might be fishy.The guide also talks about things like auditor independence, which means auditors have to be completely unbiased and not have any conflicts of interest with the company they're auditing. It's like if a detective was best friends with the suspect they were investigating – that wouldn't be fair or objective, right?Another important part of the guide covers audit risk, which is the chance that an auditor might miss something important or make a mistake in their audit. It's like if a detective overlooked a crucial piece of evidence at a crime scene. The guide helpsauditors identify and manage these risks so they can do their jobs as thoroughly as possible.Now, you might be wondering, "Why do we need all these rules and guidelines for auditors?" Well, just like you need rules in your classroom to keep things organized and fair, these auditing standards help ensure that companies are being honest about their finances. If companies weren't audited properly, they could try to hide money or lie about their profits, which could hurt investors, employees, and even the whole economy!So, the next time you see a news story about a company getting in trouble for financial misdeeds, remember that auditors and this important guide play a huge role in catching those kinds of shenanigans. By following the Auditing Standards Application Guide, auditors can be like super-detectives who keep the financial world in check and make sure everyone is playing by the rules.And who knows, maybe one day you'll grow up to be an auditor yourself, using this guide to fight financial crime and keep companies honest. But for now, just focus on following your teacher's rules in class, and you'll be well on your way to becoming a responsible citizen!篇4The Big Book of Rules for Checking the NumbersHi there! My name is Audrey and I'm going to tell you all about the really important rules accountants have to follow when they check a company's financial records. It's kind of like a big rule book that helps them do their jobs properly. Are you ready? Let's go!First up, we have the Ethics rules. These rules remind accountants to always be honest, keep things fair, stay independent from the companies they check up on, and maintain professional behavior. It's kind of like the rules your teacher has about being a good student and treating everyone with respect. The accountants have to prove they follow these Ethics rules before they can even start their work.Next, there are the big Risk Assessment rules. This part is all about understanding the company really well before digging into the numbers. The accountants need to learn about the type of business, any risks it might face, the internal controls it has to prevent mistakes or fraud, and anything else that could affect the financial statements. It's like a detective gathering all the background information before investigating a crime scene.Then we get into the really meaty stuff - the Audit Evidence rules. These tell the accountants exactly what kinds of proof they need to collect to back up the numbers in the financial reports. Things like inspecting physical inventory, confirming balances with banks, testing calculations, and examining contracts or other legal documents. It's like showing your work on a math test so the teacher knows you didn't just guess!There are also special rules for different areas like cash, inventory, investments, revenues, expenses, and so on. The accountants have to follow the correct procedures for each section. For example, the revenue rules tell them how to make sure a company properly recorded all its sales and didn't overstate its income. It's kind of like having a playbook with specific strategies for different situations in a game.Now for the hard part - if the accountants find errors or issues, they have to communicate that based on the Communication rules. Depending on how serious it is, they might have to tell the company's audit committee, update their reports, or even quit the whole audit engagement. They have to be really careful about explaining the problems clearly.There are a lot more rules in this big book, but those are some of the key chapters. The accountants basically use it as aguide to plan their work, gather evidence, and wrap things up properly. Following the rules helps give investors and the public confidence that a company's financial statements are accurate and trustworthy.Anyway, I hope this helped explain it in a simple way. Studying can be tough, but just take it step-by-step like the auditors do. Who knows, you might end up being an awesome accountant superhero someday! Now if you'll excuse me, I need to go audit my puppy's treat stash...篇5Title: Let's Learn About Auditing Standards for Accountants in China!Hey there, kids! Have you ever wondered what it's like to be an accountant? It's a pretty cool job where you get to work with numbers and help businesses keep track of their money. But did you know that accountants in China have to follow special rules called auditing standards? These standards are like a big guidebook that tells them how to do their job properly.Imagine you're playing a game, and you need to follow certain rules to win. Well, the auditing standards are kind of like that, but for accountants. They're a set of instructions that helpaccountants make sure they're doing their job correctly and honestly.So, what are these auditing standards all about? Let me break it down for you!First of all, the auditing standards are created by a group of really smart people called the Chinese Institute of Certified Public Accountants (CICPA). They're like the bosses of all the accountants in China, and they make sure everyone is playing by the same rules.The auditing standards cover all sorts of things that accountants need to do when they're checking a company's financial records. For example, they tell accountants how to plan their work, how to gather evidence, and how to report their findings.One of the most important things the auditing standards say is that accountants have to be independent and honest. That means they can't take bribes or do anything that might make them favor one company over another. They have to be fair and impartial, just like a good referee in a sports game.Another big part of the auditing standards is about risk assessment. Accountants have to look for any risks or problemsthat could affect a company's finances. It's like being a detective and searching for clues that something might be wrong.The auditing standards also talk about how accountants should communicate with the companies they're auditing. They need to ask lots of questions and share their findings with the people in charge. That way, everyone is on the same page, and the company can make any necessary changes.But wait, there's more! The auditing standards cover all kinds of other topics, like how to use technology in auditing, how to deal with special situations like fraud or legal problems, and how to report on things like environmental issues or social responsibility.Phew, that's a lot of information, right? But don't worry; accountants don't have to memorize everything all at once. The auditing standards are like a big reference book that they can go back to whenever they need help or have questions.So, why are these auditing standards so important? Well, they help make sure that companies in China are being honest about their finances. That's really important for investors, customers, and everyone else who depends on those companies. It's like having a trustworthy referee in a game, making sure everyone plays by the rules.Isn't it cool to know that there are special guidelines in place to help accountants do their jobs properly? Next time you see an accountant, you can think about all the hard work they're doing to follow the auditing standards and keep businesses running smoothly.Who knows, maybe someday you'll even want to become an accountant yourself and learn all about these auditing standards! But for now, just remember that they're like a big rulebook that helps accountants stay honest and do their jobs the right way.篇6The Awesome Auditing Adventure GuideHi there, awesome auditing adventurers! Are you ready to learn all about the super cool world of auditing? Get ready to put on your detective hats and explore the exciting rules that accountants follow when checking a company's books.First up, let's talk about what auditing actually means. You see, companies have to keep track of all their money coming in and going out - things like sales, expenses, payments to workers, and so on. Auditors are like financial detectives who make sure the numbers add up properly and that everything is on theup-and-up.In China, there are special standards that auditors have to follow to do their jobs right. These are called the Chinese Certified Public Accountant Auditing Standards. They act like a guidebook filled with important rules and steps that auditors need to take when auditing a company. It's kind of like how adventurers need to follow a treasure map to find the loot!The first big rule is about being independent and honest. Auditors have to be like fair judges - they can't take sides or be influenced by anyone. Their job is to look at the evidence and financial records objectively without any bias. It's like being an umpire at a baseball game - you call it like you see it, no favors for anyone!Next up is having the right professional skills and knowledge. Auditors need to be total math whizzes who understand all the accounting rules backward and forward. They also have to stay up-to-date on the latest auditing procedures. Companies' finances can get super complex, so auditors have to be financial experts!Planning is another crucial part of the auditing process. Just like how you'd plan a trip to the beach - packing your swimsuit, grabbing some snacks, etc. - auditors need to properly plan out their work. They figure out what areas to focus on, whatdocuments they need to look at, what risks to watch out for, and how to gather all the evidence they need. Skipping this planning stage would be like going to the beach without sunscreen - you're gonna get burned!During the actual audit work, auditors have to gather lots and lots of evidence to back up their conclusions. They pore over financial statements, accounting records, contracts, invoices, and more. It's like being a detective, gathering clues and piecing together the whole picture. Auditors have to be superdetail-oriented to catch anything fishy.Communicating is key too. Auditors share important findings with the company they're auditing and discuss any issues that come up. They have to be clear educators to explain complex accounting standards in simple terms. At the end, they provide their official auditing report and opinion on whether the company's financial records are accurate.All along the way, auditors have to create and keep incredibly thorough documentation on everything they did, found, and concluded. These audit working papers act like a trail of breadcrumbs, allowing anyone to re-trace the auditor's steps. It's how they demonstrate they followed all the auditing rules to a T.Finally, the auditing standards require auditors to continue improving through quality control reviews. Their work gets evaluated by more experienced auditors to see if they missed anything or if there are areas they can learn from. It's like getting coaching advice after a big game to up your skills for next time.Phew, that's a lot to take in! Auditing is a seriously important job with tons of complicated standards and procedures to follow. By adhering to guidelines like these, auditors promote transparency and keep the financial world in order.So thanks for joining me on this auditing adventure! I know it was a long and complex trail to navigate, but I hope you walked away with a basic understanding of these essential accounting rules. Stay curious, study hard, and who knows - you may become a top-notch auditing detective yourself one day! The corporate world needs honest auditing experts to keep things in check. Why not let that be your awesome future job?。

本科毕业论文(设计)外文翻译外文题目Independent Review Organizations Must Meet GAOYellow Book Standards外文出处Journal of Health Care Compliance,2010(2):27-32外文作者Herrmann Thomas E原文:Independent Review Organizations Must Meet GAO “Yellow Book”StandardsBACKGROUNDOn July 30, 2001, the OIG, in conjunction with the Health Care Compliance Association (HCCA), cosponsored a Government Industry Roundtable to discuss “issues surrounding the implementation and maintenance of effective compliance programs.” Specifically addressed in the discussion was the OIG’s requirement, in the context of health care fraud and abuse settlements, that an IRO be retained by a health care entity to perform annual billing, systems, and/or other compliance reviews. Participants recognized that:The OIG requires IROs because the OIG does not have the resources to conduct the level of review necessary to determine if a provider is meeting the requirements of the CIA as well as other Federal health care program requirements. Additionally, a review by an independent entity provides the OIG with assurances that a provider’s compliance program and billing systems are objectively reviewed.Roundtable participants referenced a number of advantages associated with using an IRO. “IROs provide a broad industry perspective and expertise, are independent, help identify system weaknesses, make helpful recommendations, and their reviews serve as a useful benchmark for future reviews conducted by the provider.”OIG REQUIREMENTS FOR IRO INDEPENDENCEThe obligations for an audit/review organization, such as an IRO, to meet “independence”standards are referenced in GAGAS as set forth by the GAO in its “Yellow Book.” These standards are applicable to financial audits, typically performed by certified public accountants (CPAs), attestation engagements, and performance audits, which may be undertaken by professionals such as consultants and lawyers. The great majority of CIAs does not mandate financial audits but are rather focused on performance audits, i.e., those involving claims, systems, or arrangements with referral sources that may implicate the anti-kickback statute and Stark law.From the perspective of the OIG, it is essential that an IRO conduct its reviews with both independence and objectivity. A standard requirement in an OIG CIA is that “[t]he IRO must perform [its] review in a professionally independent and objective fashion, as appropriate to the nature of the engagement, taking into account any other business relationships or engagements…” Typically, the IRO is obligated to provide a certification regarding its professional independence and objectivity. Further, the usual CIA specifi es that “i n the event OIG has reason to believe that the IRO…is not independent and objective…, the OIG may, at its sole discretion, require” the engagement of a new IRO.The OIG has stated that an IRO should follow “the standards for auditor independence set forth in the General Accounting Office (GAO), Government Auditing Standards (2003 Revision).” The OIG has indicated that, under these standards, “CIA reviews would be considered performance audits and IROs would be subject to the independence standards set forth in the Yellow Book that relate to performance audits.” In referencing the GAO Yellow Book’s applicability to IRO independence, the OIG has further noted:When assessing independence, the two overarching principles that must be considered are that: audit organizations should not perform management functions or make management decisions; and audit organizations should not audit their own work or provide non-audit services in situations where the non-audit services are signify- cant/material to the subject matter of the audits.THE GAO YELLOW BOOK STANDARDSThe GAO Yellow Book, first issued by the Comptroller General of the United States in 1972, is intended to:Address the unique requirements of governmental entities;Establish general standards for both governmental and nongovernmental auditors performing audits in accordance with GAGAS;Supplement field work and reporting standards of the American Institute of certified Public Accountants (AICPA) Auditing Standards Board;Establish field work and reporting standards for performance audits.In July 2007, the GAO issued its fourth revision of the Yellow Book standards.With respect to performance audits, such as those performed by IROs, the new standards are applicable to those undertaken on or after January 1, 2008.The latest edition of the Yellow Book reinforces the principles of transparency, accountability, and quality in government auditing. There is an increased emphasis placed on governing ethical principles, clarification of the impact of performing nonaudit services on auditor independence, and enhancement of performance audit standards. In issuing the 2007 edition, Comptroller General David M. Walker noted that the revision sets forth “changes from the 2003 revision that reinforce the principles of transparency and accountability and provide the framework for high-quality government audits that add value.” A summary of the key Yellow Book principles that are applicable to performance audits undertaken by IROs, pursuant to CIAs, follows.e and Application of GAGASChapter one of the revised Yellow Book highlights GAGAS requirements and states that they “provi de a framework for conducting high quality government audits and attestation engagements with competence, integrity, objectivity, and independence.”It notes further that “GAGAS contain re quirements and guidance dealing with eth ics, independence, auditors’ professional compe tence and judgment, quality control, the performance of field work, and reporting.” It explains: Performance audits are defined as engagements that provide assurance orconclusions based on an evaluation of sufficient appropriate evidence against stated criteria, such as specific requirements, measures, or defined business practices. Performance audits provide objective analysis so that management and those charged with governance and oversight can use the information to improve program performance and operations, reduce costs, facilitate decision making by parties with responsibility to oversee or initiate corrective action, and contribute to public accountability.For performance audits, such as those undertaken by IROs, the revised Yellow Book indicates that certain other standards also may be utilized by reviewers in conjunction with GAGAS:International Standards for the Professional Practice of Internal Auditing;Guiding Principles for Evaluators;The Program Evaluations Standards; andStandards for Educational and Psychological Testing.2. Ethical PrinciplesChapter two of the revised Yellow Book sets forth ethical principles to provide a foundation, discipline, and structure for an audit/review entity in applying GAGAS. It notes that “e thical principles apply in preserving auditor independence, taking on only work that the auditor is competent to perform, performing high-quality work, and following the applicable standards cited in the audit report.” Further, “i ntegrity and objectivity are maintained when auditors perform their work and make decisions that are consistent with the broader interest of those relying on the auditors’ report, including the public.”The following ethical principles are specified as guiding the work of reviewers and auditors and need to be both considered and addressed by an organization serving as an IRO:The public interest;Integrity;Objectivity;Proper use of government information, Resources, and position; andProfessional behavior.3. General StandardsChapter three of the revised Yellow Book specifies general standards applicable to performing audits and reviews consistent with GAGAS. These standards focus on: Independence of the audit organization and individual auditors;The exercise of professional judgment in the performance of work;The competence of auditors/reviewers; andQuality control and assurance, as well as external peer review.While all of these factors are critical to activities of an IRO, of fundamental import ance is the concept of “independence.” “The audit organization and individual a uditor…must be free from person al, external, and organizational impairments to independence, and must avoid the appearance of such impairments to independence.” The importance of “independence” is further highlighted:Auditors and audit organizations must maintain independence so that their opinions, findings, conclusions, judgments, and recommendations will be impartial and viewed as impartial by objective third parties with knowledge of the relevant information. Auditors should avoid situations that could lead objective third parties with knowledge of the relevant information to conclude that the auditors are not able to maintain independence and thus are not capable of exercising objective and impartial judgment on all issues associated with conducting the audit and reporting on the work.Key challenges to auditor independence are personal impairments, external impairments, and organizational independence. Critical to assessing “organizational independence” is determining whether the au dit organization also performs other professional, or nonaudit, services for the audited entity. The Yellow Book advises that:External audit organizations can be presumed to be free from organizational impairments to independence when the audit function is organizationally placed outside the reporting line of the entity under audit and the auditor is not responsible for entity operations.The revised Yellow Book sets forth two basic principles for determining auditor independence when assessing the impact of performing a nonaudit service for an audited entity:The audit organization must not provide nonaudit services that involve performing management functions or making management decisions; and The audit organization must not audit its own work or provide nonaudit services in situations in which the nonaudit services are significant or material to the subject matter of the audit.In the context of these “overarching principles,” the OIG has identified certain situa tions in which an IRO’s independence might be compro mised because of its prior relationship and work for an audited provider:If the provider were to outsource its internal compliance audit function to the IRO, either before or after the execution of the provider’s CIA, the IRO’s independence likely would be impaired for purposes of conducting the provider’s CIA reviews. This is the case because internal audit is a management function and the outsourcing of the internal compliance audit function likely would result in the IRO auditing its own work as part of the CIA reviews.The OIG has stated that the most important consideration in assessing IRO indepen dence “is whe ther the IRO is involved in performing a management function or making management decisions for the provider.” It notes that “if the IRO participates in any form of decision-making…the IRO likely would be precluded from performing the CIA reviews because the IRO is in the position of making managemen t decisions for the provider.”4. Field Work Standards for Performance AuditsChapter seven of the revised Yellow Book sets forth field work standards and provides guidance for performance audits conducted. These standards include planning the audit, supervising staff, obtaining sufficient and appropriate evidence, and preparing audit documentation. Critical to establishing and following these standards are the following concepts:Reasonable assurance;S ignificance; andAudit risk.A performance audit, such as an IRO re view, must “provide reasonable assurance that evidence is sufficient and appropriate to support the auditors’ findings and conclusions.”“Significance is defined as the relative importance of a matter with the context in which it is being considered, including quantitative and qualitative factors.”Audit risk is “the possibility that the auditors’ findings, conclusions, recommendations, or assurance may be improper or inco mplete.”Thus, the IRO, in planning and conducting its review, must be cognizant of these factors and ensure that the review process and findings are in accord with these principles.5. Reporting Standards for Performance AuditsChapter eight of the revised Yellow Book sets forth the form of the report, the report contents, report issuance, and distribution. Critical to issuance of an IRO report is the presentation of “sufficient, appropriate evidence to support the findings and conclusions in relation to the audit objectives.”The OIG has expressly adopted the GAO Yellow Book standards as governing IROs. Accordingly, the current Yellow Book provisions need to be carefully reviewed and followed by a health care entity in selecting an organization to serve as an IRO. Moreover, the Yellow Book standards need to be recognized and followed by an IRO in conducting its activities.Critical to successful compliance with the terms of a CIA with the OIG is ensuring that mandated IRO reviews are conducted in an independent, objective, and comprehensive manner. This is necessary to provide assurances to the government that a health care entity is qualified, capable, and competent to continue participating in federal health care programs. Both the OIG and the subject health care entity are reliant up on an IRO’s commitment and capa bility to conduct its reviews in accordance with GAGAS. Therefore, the Yellow Book standards must be recognized and adhered to by the IRO retained by a health care entity subject to an OIG CIA. In light of this, any health care entity that is subject to a CIA should address the following questions when selecting an IRO:Does a review organization have knowledge of and past experience in applying the GAGAS requirements to its audits and reviews?Are there any constraints on an organi zation’s independence and objectivity in conducting OIG-mandated reviews as set forth in a CIA, either in terms of past or current engagements with the health care organization or other industry activities?Does the audit/review organization have the capability, capacity, and competence to perform the OIG-required performance audits, e.g., claims, systems, or arrangements review?Does the organization have quality control and assurance procedures to ensure the reliability and integrity of its audits/reviews?Can the audit/review organization certify and attest that it has conducted its review in accordance with GAGAS, as set forth in the revised Yellow Book?Source:Herrmann Thomas E.Independent Review Organizations Must Meet GAO Yellow Book Standards[J].Journal of Health Care Compliance,2010(2):27-32.译文:独立的审计机构必须符合“黄皮书”的指标背景2001年7月30日,监察会同HCCA进行了一次商洽,共同探讨怎样实现和维护有效的合规计划。

总体评价:本次考试包括5个必答题。

A部分包括30分的问题1和10分的问题2。

B 部分包括三个更深入的问题,每题20分。

大部分考生完成了5个题目,然而还是有少部分没有完成问题的考生,这表明考试是有时间压力的。

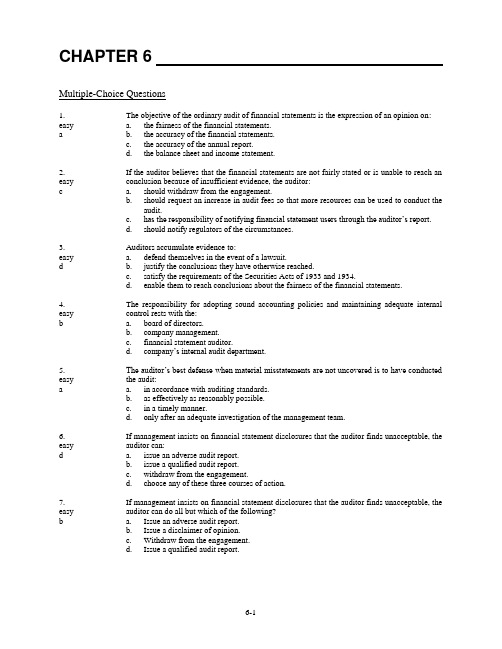

General CommentsThe examination consisted of five compulsory questions.Section A contained question 1 for 30 marks and question 2 for 10 marks.Section B comprised three further questions of 20 marks each.The majority of candidates completed all five questions;however there was some evide nce of time pressure as a significant minority of candidates did not attempt all questions.T his seemed to mainly occur for question 5 or for the questions candidates found challengi ng,which are listed below.In addition a significant minority answered question 1 last and t heir answers were often incomplete.As question 1 is the case study and represents 30 of t he available marks,leaving this question until last can be a risky strategy,as many answers presented were incomplete or appeared rushed.Candidates performed particularly well on questions 1b,2c,3ci and 4bi.The questions c andidates found most challenging were questions 1a,2b,3a,3cii and 5b.This was mainly due to a combination of failing to read the question requirement carefully and insufficient kn owledge.A number of these areas were new to the F8 study guide in 2010 and hence as new topic areas should have been prioritised by candidates.A number of common issues arose in some candidate’s answers:•Failing to read the question requirement clearly and therefore providing irrelevant ans wers which scored few if any marks•Providing more than the required nu mber of points•Illegible handwriting and poor layout of answers.Specific CommentsQuestion OneThis 30-mark question was based on a retailer of ladies clothing and accessories,Grey stone Co,and tested candidates’ knowledge of internal control defi ciencies,trade payables an d internal audit.Part (a) for 5 marks required candidates to explain examples of matters that the audit or should consider in determining whether an internal control deficiency was significant.This part of the question was unrelated to the Greystone Co scenario and hence teste d candidates’ knowledge as opposed to application skills.This question related to ISA 265 Communicating Deficiencies in Internal Control to those Charged with Governance and Ma nagement,which is a new ISA and new to the F8 study guide for 2010.Most candidates performed inadequately on this part of the question.The main reason for this is that candidates failed to read the question properly or did not understand what the requirement entailed.The question asked for matters which would mean internal control deficiencies were significant enough to warrant reporting to those charged with governanc e.The question was not asking for examples of significant internal control deficiencies,how ever this is what a majority of candidates gave.Many answers included a long list of cont rol deficiencies such as “inadequate segregation of duties” this failed to score marks as it was not answering the question.It was apparent that many candidates had not studied the area of significant control d eficiencies,and as there is now an ISA dedicated to this area,this was unsatisfactory.Part (b) for 14 marks required a report to management which identified and explained four deficiencies,implications and recommendations for the purchasing system of Greyston e Co.A covering letter was required and there were 2 presentation marks available.This part of the question was answered well by the vast majority of candidates with some scoring full marks.The scenario was quite detailed and hence there were many possi ble deficiencies which could gain credit.Where candidates did not score well this was mai nly due to a failure to explain the deficiency and/or the implication in sufficient detail.So me candidates simply listed the information fr om the scenario such as “purchase invoices are manually matched to GRNs” and then failed to explain the implication of this for Gre ystone Co.A significant minority also failed to score marks because they provided deficiencies w hich were unrelated to the purchasing system,such as “internal audit’s only role is to perf orm inventory counts.” This was outside the scope of the question requirement and hence did not gain credit.Candidates are once again reminded that they must read the question r equirements carefully.Many candidates failed to score the full 2 marks available for presentation as they di d not produce a covering letter.A significant minority just gave the deficiencies,implication s and recommendations without any letter at all;this may be due to a failure to read the question properly.Also even when a letter was produced this was often not completed.Candidates would provide the letterhead and introductory paragraph,the detail of the d eficiencies,implications and recommendations,but then they would fail to include a concludi ng paragraph and letter sign off which would have earned a further 1 mark.In addition so me candidates produced a memo rather than a letter.In general,where candidates adopted a columnar approach to their answer they tended to score well.The question asked for four deficiencies,implications and recommendations,however ma ny candidates provided much more than the required four points.It was not uncommon to see answers which had six or seven points.Whilst it is understandable that candidates wish to ensure that they gain credit for four relevant points,this approach can lead to time pre ssure and subsequent questions can suffer.Part (c) for 5 marks required substantive procedures the auditor should perform on ye ar-end trade payables.This was answered satisfactorily for many candidates.The most comm on mistake made by some candidates was to confuse payables and purchases and hence pr ovide substantive tests for purchases such as “agree purchase invoices to goods received n otes”.As there was no reference to year-end payables then this test would not have scored any marks.A minority provided tests of controls as well as substantive procedures and ag ain these would not have scored any marks.The requirement verb was to “describe” th erefore sufficient detail was required to sco re the 1 mark available per test.Candidates are reminded that substantive procedures is a c ore topic area and they must be able to produce relevant detailed procedures.Answers such as “discuss with management to confirm ownership of payables” is far too vague to gain credit as there is no explanation of what would be discussed and also how such a discus sion could even confirm ownership.Part (d) for 5 marks required additional procedures the internal auditors of Greystone Co could perform;this was in addition to their current role of performing regular inventory counts.This required candidates to use their knowledge of internal audit assignments and apply it to a retailer scenario.On the whole candidates performed satisfactorily on this que stion.Many were able to identify assignments such as value for money audits,reviewing int ernal controls,assisting the external auditors and other operational internal audits.However s ome candidates restricted their answers to assignments the auditors would perform in light of the control deficiencies identified in part (b) of their answer.This meant that their ans wers lacked the sufficient breadth of points required to score well.问题二包括了“真实和公允”原则、国际审计准则以及审计文件。

有关审计报告的审计准则英文版Auditing standards, also known as Generally Accepted Auditing Standards (GAAS) in the United States, are a set of systematic guidelines used by auditors when conducting audits of a company's financial information. 审计准则,也被称为美国的一般受理审计准则(GAAS),是审计师在对公司财务信息进行审计时所使用的一套系统性指导方针。

These standards are used to ensure that auditors perform their duties with integrity, objectivity, and professional competence. 这些标准用于确保审计师在履行职责时具有诚信、客观性和专业能力。

The auditing standards serve as a framework for auditors to follow in order to provide a reasonable assurance that the financial statements of a company are free from material misstatement. 审计准则作为审计师所要遵循的框架,旨在提供合理保证,即公司的财务报表不存在重大错误陈述。

By adhering to these standards, auditors are able to maintain consistency and reliability in their audit work across different companies and industries. 通过遵守这些标准,审计师能够在不同公司和行业的审计工作中保持一致性和可靠性。

C LIENTM EMORANDUM PCAOB APPROVES FINAL STANDARD FOR AUDITOR ATTESTATIONS OF INTERNAL CONTROL OVER FINANCIAL REPORTINGThe Public Company Accounting Oversight Board (the “PCAOB”) recently approved a final standard for auditor attestations of a company’s internal control over financial reporting. These attestations are required under Section 404 of the Sarbanes-Oxley Act of 2002 in connection with management’s assessment of such internal control.Management Assessment of Internal Control Over Financial ReportingPursuant to Section 404 of the Sarbanes-Oxley Act, on June 5, 2003, the Securities and Exchange Commission (the “SEC”) adopted final rules requiring management of a reporting company to assess the effectiveness of the company’s internal control over financial reporting1 as of the end of the company’s most recent fiscal year and to describe in the company’s annual report management’s conclusion, as a result of that assessment, whether the company’s internal control is effective. The rules require that management’s internal control report state that the registered public accounting firm that audited the company’s financial statements has issued an attestation report as to whether management’s assessment of the company’s internal control over financial reporting is “fairly stated in all material respects.” The company must then file the attestation report as part of its annual report.Companies that are “accelerated filers” (generally Form S-3 eligible companies) must comply with these requirements in their annual reports for their first fiscal year ending on or after November 15, 2004; non-accelerated filers and foreign private issuers must comply with these requirements in their annual reports for their first fiscal year ending on or after July 15, 2005. The Sarbanes-Oxley Act further directed the PCAOB to establish professional standards governing the independent auditors’ attestation report. Accordingly, on March 9, 2004, following a previously proposed version, the PCAOB adopted Auditing Standard No. 2, An Audit of Internal Control Over Financial Reporting Performed in Conjunction With an Audit of Financial Statements (“Auditing Standard No. 2”). This Standard has been submitted to the SEC for its approval.1The SEC defines “internal control over financial reporting” as a “process designed by, or under the supervision of, the issuer’s principal executive and principal financial officers . . . to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements” in accordance with GAAP. It includes policies and procedures for maintaining accounting records, recording transactions, authorizing receipts and expenditures and safeguarding assets.Audit of Internal Control Over Financial ReportingAlthough the work required to be performed by the independent auditors is referred to as an “attestation,” the PCAOB has stated that the attestation engagement requires the same level of work as an audit of internal control over financial reporting. Consequently, Auditing Standard No. 2 requires that the auditors not just evaluate the adequacy of management’s processes for assessing the effectiveness of the company’s internal control over financial reporting, but that the auditors independently test the effectiveness of the internal control itself.Because of the similar objectives and work involved in audits of internal control over financial reporting and audits of financial statements, the PCAOB decided that these two audits should be integrated. Accordingly, the auditors who conduct the audit of internal control over financial reporting must also audit the company’s financial statements. The two audit reports may be separate or combined, but should be dated the same date.The requirements in Auditing Standard No. 2 are based on the internal control framework established by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”). However, Auditing Standard No. 2 allows companies flexibility in choosing an alternative framework that encompasses all of COSO’s general themes.Commentary:Ø The COSO framework consists of five interrelated components: control environment (so-called “tone at the top”), risk assessment, control activities toensure that management directives are carried out, capture and communication ofinformation and monitoring activities.Ø Although the COSO framework addresses the effectiveness and efficiency of operations and compliance with applicable law as well as the reliability offinancial reporting, the SEC’s requirements regarding internal control overfinancial reporting focus on the latter category. However, controls on operationsand compliance with law, to the extent they may affect financial reporting, arealso part of the SEC’s requirements.Ø Auditing Standard No. 2 provides the auditors with some flexibility to use work performed by others, including the internal auditors and management’sassessment. The more extensive and reliable the work is, and the betterdocumented it is, the less extensive and costly the independent auditors’ workwill need to be. Still, the independent auditors’ own work must constitute theprincipal evidence, both quantitative and qualitative, for their audit opinion.Ø Embedded in the SEC definition of “internal control over financial reporting” is that management’s assessment of the company’s internal control must provide“reasonable assurance” of its effectiveness. The definition recognizes that thecontrol processes will reduce, but not eliminate, the risk of financial reportingissues.Management’s ResponsibilitiesFor the auditors to perform their audit of the internal control, management must: • accept responsibility for the effectiveness of the company’s internal control over financial reporting;• evaluate the effectiveness of the internal control using acceptable criteria;• support its evaluation with sufficient evidence, including documentation; and• present its written assessment of the effectiveness of the company’s internal control as of the end of the fiscal year.If the auditors conclude that management has not satisfied these responsibilities, they should communicate, in writing, to management and the audit committee that the audit cannot be completed.The Audit ProcessThe audit of internal control over financial reporting is an extensive process involving multiple steps. These steps include planning the audit, evaluating the process that management used to perform its assessment of the effectiveness of the internal control, evaluating the effectiveness of both the design and operation of the internal control and forming an opinion about whether the internal control is effective.In addition to testing management’s assessment process and the work on internal control by others, such as the internal auditors, the auditors must test the internal control directly. For example, the auditors are required to perform walkthroughs in each annual audit to trace transactions from origination, through the company’s accounting and information systems and financial report preparation processes, to their being reported in the company’s financial statements.Auditing Standard No. 2 emphasizes the importance of controls over possible fraud and requires the auditors to test controls specifically intended to prevent, deter and detect fraud. These controls start with the “tone at the top” and include, for example, controls to prevent the misappropriation of assets, risk assessment processes, codes of ethics, internal audit activities and audit committee oversight and whistleblower procedures.Commentary:Ø More limited procedures are required to be performed by the auditors in connection with management’s quarterly certifications regarding internal controlrequired under Section 302 of the Sarbanes-Oxley Act.Auditor IndependenceUnder Rule 2-01 of Regulation S-X, the auditors’ independence is compromised if the auditors audit their own work or act as management, such as by designing or implementing the internal control. These restrictions, however, do not preclude the auditors from making recommendations as to how management may improve the design or operation of the internal control as a by-product of an audit.Auditing Standard No. 2 prohibits the auditors from providing any internal control-related service, unless the service has been specifically pre-approved by the audit committee (rather than through a general categorical approval). At all times, management must be actively involved and retain responsibility for the control matters.Timing of TestingThe Sarbanes-Oxley Act requires management’s assessment and the auditor’s opinion to address whether the internal control was effective as of the end of the company’s most recent fiscal year. Obviously, performing all of the testing on December 31 is neither practical nor appropriate. Auditing Standard No. 2 recognizes that to express an opinion about whether the internal control was effective as of a point in time the auditors must obtain evidence that the internal control operated effectively over an appropriate period of time. Accordingly, the Standard provides that the auditors should obtain evidence about operating effectiveness at different times throughout the year and then update those tests at the end of the year.Commentary:Ø Controls “as of” a specific date include controls relevant to financial reporting “as of” that date, even if they may not operate until later. For example, certaincontrols over the period-end financial reporting process normally operate onlyafter the end of the period.Evaluating the Results of TestingAuditing Standard No. 2 differentiates among a control deficiency, a significant deficiency and a material weakness:• A control deficiency exists when the design or operation of a control does not allow the company’s management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis.• A control deficiency is classified as a significant deficiency if, by itself or in combination with other control deficiencies, it results in more than a remote likelihood that a misstatement of the company’s annual or interim financial statements that is more than inconsequential will not be prevented or detected.• A significant deficiency is classified as a material weakness if, by itself or in combination with other control deficiencies, it results in more than a remote likelihood that a material misstatement in the company’s annual or interim financial statements will not be prevented or detected.The auditors must evaluate the severity of all control deficiencies, communicate such deficiencies in writing to management and notify the audit committee that such communication has been made. All significant deficiencies and material weaknesses must also be communicated in writing to the audit committee.Auditing Standard No. 2 provides examples of circumstances that are significant deficiencies, as well as strong indicators of the existence of a material weakness, including:• ineffective oversight of the company’s external financial reporting and internal control over financial reporting by the company’s audit committee;Commentary:Ø Ironically, this means that the independent auditors, who are hired and supervised by the audit committee, must evaluate the effectiveness of theiroverseers.• any material misstatement in the financial statements not initially identified by the company’s internal control;• significant deficiencies that have been communicated to management and the audit committee, but that remain uncorrected after reasonable periods of time;• ineffective internal audit or risk assessment functions, particularly for large or complex companies;• an ineffective regulatory compliance function in regulated companies, where violations of applicable law could have a material effect on financial reporting; and • identification of fraud of any magnitude by senior management.Forming an Opinion and ReportingSimilar to management’s internal control report, only material weaknesses are required to be disclosed in the auditors’ report on the effectiveness of the control. If the auditors have identified a material weakness, they must conclude that the company’s internal control is not effective; a qualified opinion is not permitted if there is a material weakness.Auditing Standard No. 2 permits the auditors to express an unqualified opinion only if the auditors have not identified any material weaknesses in the internal control after having performed all of the procedures that the auditors consider necessary under the circumstances. Ifthe auditors cannot perform all necessary procedures, they are required to qualify or disclaim their opinion.Auditing Standard No. 2 further requires that the auditors report on management’s assessment of the internal control. In the event of a material weakness, the auditors could express an unqualified opinion on management’s assessment so long as management properly identified the material weakness and concluded in its assessment that the internal control was not effective. If the auditors and management disagree about the existence of a material weakness, then the auditors must render an adverse opinion on management’s assessment.ImplementationGiven the extensive amount of time required to evaluate a company’s internal control procedures and then design, implement and test any additional procedures that may be required, companies should already be well on their way in evaluating and implementing these requirements and preparing for management’s internal control report and the related auditors’ attestation report.Commentary:Ø Even though the independent auditors do not need to provide their attestation report until after year-end, make sure to involve them in the ongoing evaluationand testing processes to help ensure that there are no last minute surprises.Ø Pay attention to these requirements in connection with any business acquisition, particularly at the end of the year and particularly of private companies, whichmay not have the controls required of public companies. With no transitionperiod for newly acquired entities, any acquisition will need to be included aspart of the review of internal controls for the year in which the acquisition isconsummated. If necessary, consider adjusting the closing date.Ø Companies will need to obtain the auditors’ consent to the incorporation by reference of their attestation report in connection with any registration statementfiled under the Securities Act, similar to auditor consents to the incorporation oftheir report on the financial statements. As with the auditor consent regardingtheir report on the financial statements, this consent regarding their attestationreport will require that management deliver an updated representation letter tothe auditors.* * * * * * * * * * *If you wish to obtain additional information regarding this new PCAOB standard and related SEC regulations regarding management’s internal control report, please contact Serge Benchetrit, John S. D’Alimonte, Steven J. Gartner, Yaacov M. Gross, Jeffrey S. Hochman or the corporate partner with whom you regularly work. For help with a current investigative or regulatory issue, feel free to call litigators Stephen W. Greiner, Richard L. Posen or Michael R. Young of our Accounting Irregularities Practice Group.Willkie Farr & Gallagher LLP is headquartered at 787 Seventh Avenue, New York, NY 10019-6099. Our telephone number is 212-728-8000, and our facsimile number is 212-728-8111. Our website is located at .March 30, 2004Copyright © 2004 by Willkie Farr & Gallagher LLP.All Rights Reserved. This memorandum may not be reproduced or disseminated in any form without the express permission of Willkie Farr & Gallagher LLP. This memorandum is provided for news and information purposes only and does not constitute legal advice or an invitation to an attorney-client relationship. While every effort has been made to ensure the accuracy of the information contained herein, Willkie Farr & Gallagher LLP does not guarantee such accuracy and cannot be held liable for any errors in or any reliance upon this information.。

certified audit standardCertified Audit Standard: Enhancing Transparency and AccountabilityIntroductionIn today's complex business environment, financial reporting and disclosure play a critical role in ensuring trust and confidence among stakeholders. Companies are required to provide accurate and reliable financial information to their shareholders, investors, and regulators. To meet these expectations, auditors play a crucial role in evaluating and certifying the financial statements of organizations. The certified audit standard, a set of guidelines and principles, helps auditors perform their duty with professionalism and integrity. This article will delve into the certified audit standard, its purpose, key components, and its significance in enhancing transparency and accountability.Understanding the Certified Audit StandardThe certified audit standard is a framework that outlines the principles and procedures to be followed by auditors whileconducting an audit. This standard sets out the guidelines for an independent, objective, and systematic examination of financial records, statements, and internal controls of an organization. The objective is to express an opinion on the fairness and accuracy of the financial statements being audited.Key Components of the Certified Audit Standard1. Independence and Objectivity: The certified audit standard emphasizes that auditors must remain independent and neutral throughout the audit process. They should have no personal or financial interest in the organization being audited, ensuring their objectivity and ability to form an unbiased opinion.2. Professional Competence: The standard requires auditors to possess the necessary knowledge, skills, and expertise to carry out the audit effectively. They should stay updated with the latest accounting principles, auditing standards, and relevant industry regulations.3. Audit Planning and Risk Assessment: Before commencing an audit, auditors must carefully plan and assess the risk involved. Thisstep involves understanding the organization's internal control system, evaluating potential risks, and designing appropriate audit procedures to mitigate those risks.4. Audit Evidence and Documentation: The certified audit standard emphasizes the importance of obtaining sufficient and appropriate audit evidence that supports the auditor's opinion. Auditors need to document their work meticulously, ensuring transparency and allowing other professionals to understand the audit procedures followed.5. Communication and Reporting: The standard requires auditors to communicate with the organization's management throughout the audit process. They should discuss any significant issues identified during the audit and provide timely and accurate reports to management, shareholders, and regulatory bodies.Significance of the Certified Audit StandardEnhancing Transparency: The certified audit standard ensures that auditors follow a systematic and consistent approach while examining the financial statements. By doing so, they enhancetransparency by providing stakeholders with accurate and reliable information about the financial health of the organization.Improved Accountability: Certification under the audit standard makes companies accountable for their financial reporting. The independent opinion provided by auditors increases the credibility of the financial statements, promoting trust among stakeholders.Minimizing Fraud and Misrepresentation: Through the certified audit standard, auditors help detect financial fraud and misrepresentation. By conducting a thorough examination of the organization's records and internal controls, auditors are better positioned to identify any irregularities or potential risks.Regulatory Compliance: The certified audit standard aligns with regulatory requirements and guidelines set by regulatory bodies such as the Public Company Accounting Oversight Board (PCAOB) in the United States. Compliance with these standards ensures that companies meet legal obligations and reporting requirements.ConclusionThe certified audit standard plays a vital role in ensuring transparency, accountability, and trust in financial reporting. By adhering to the principles and guidelines set by this standard, auditors can perform their duties efficiently and effectively. The certified audit standard acts as a benchmark for auditors, providing organizations and stakeholders with confidence in the accuracy and fairness of financial statements. Through the establishment of stringent guidelines, auditors can minimize financial fraud, enhance transparency, and contribute to a more reliable financial reporting ecosystem.。