作业成本法在制造业的应用:并与传统成本法比较【外文翻译】

- 格式:doc

- 大小:51.50 KB

- 文档页数:9

浅谈作业成本法在制造企业中的运用作业成本法(Job Costing)是一种在制造企业中常用的成本核算方法。

它通过将制造过程划分为各个作业来确定和追踪每一个作业的成本,从而帮助企业管理者更好地控制成本、评估利润和做出决策。

以下是对作业成本法在制造企业中运用的一些浅谈。

首先,作业成本法对于制造企业来说是一种很有效的成本核算方法。

在制造企业中,产品的制造过程通常会经历多个阶段和环节,每个阶段和环节都涉及到不同的资源消耗和成本产生。

作业成本法通过将制造过程划分为各个作业,将成本分配到每个作业上,从而更精确地计算出每个作业的成本,为企业管理者提供了关于各个作业成本的详细信息。

其次,作业成本法有助于企业管理者了解产品成本的组成和结构。

作业成本法将产品的制造过程分解为不同的作业,可以清晰地显示出产品成本的组成和结构。

通过对每个作业的成本进行追踪和分析,企业管理者可以了解到产品制造过程中哪些环节和因素对成本的影响最大,从而指导企业在降低成本和提高效率方面做出相应的调整和决策。

另外,作业成本法可以帮助制造企业准确计算成本和评估利润。

制造企业的产品成本通常包括直接材料成本、直接人工成本和制造间接费用等多个方面,如果没有一个准确的成本核算方法,很难确定产品的实际成本和利润。

作业成本法将成本分配到每个作业上,可以帮助企业准确计算每个作业的成本,并根据销售价格对每个作业进行定价,从而评估出每个作业的利润。

通过对每个作业的成本和利润进行监控和分析,企业可以及时采取措施来降低成本、提高利润。

最后,作业成本法为制造企业提供了基于成本的决策依据。

通过对每个作业的成本进行追踪和分析,企业可以得出每个作业的利润率和贡献率等指标,从而根据不同作业的成本和利润情况来进行决策。

例如,在产品定价方面,企业可以通过对不同作业的成本和利润进行分析,确定合理的销售价格;在资源配置方面,企业可以根据不同作业的成本和利润,合理安排资源的使用和分配;在产品开发方面,企业可以根据不同作业的成本和利润,决定是否继续开发或停产一些产品。

作业成本法与传统成本法的对比与应用在企业管理会计中,成本计算方法是非常关键的一环,而作业成本法和传统成本法是两种常用的成本计算方法。

本文将对这两种方法进行对比,并探讨它们的应用情况。

作业成本法作业成本法是一种针对特定产品或服务,以作业(或任务)为单位来计算成本的方法。

它强调对每个作业进行独立计算,可以更准确地了解每个作业的成本构成。

作业成本法适用于生产过程复杂、产品种类繁多的企业,能够更好地追踪和控制成本。

传统成本法传统成本法是一种按部门或功能对成本进行分配的方法,主要包括作业成本法和过程成本法。

传统成本法更注重整体成本,将总成本按照某种基础(如直接人工成本、直接材料成本等)分配到各个部门或产品上,适用于生产过程简单、结构清晰的企业。

对比分析成本分配方式作业成本法:成本分配更加精确,能够将成本直接关联到具体作业,便于实现精细化管理。

传统成本法:成本分配相对简单,以部门或功能为单位进行成本分配,缺乏细化的成本控制。

适用场景作业成本法:适合于生产过程复杂、产品差异性大的企业,能够更好地理解每个作业的成本分布情况。

传统成本法:更适用于生产过程相对简单、产品结构相对单一的企业,能够以较低的成本估算整体生产成本。

管理决策支持作业成本法:提供了更多关于作业绩效和成本构成的信息,有助于管理层做出更精准的决策。

传统成本法:提供了对整体成本的把控,有利于整体成本控制和绩效评价。

应用建议在对作业成本法和传统成本法进行对比的基础上,企业可以根据自身的生产特点和管理需求来选择适合的成本计算方法。

对于生产工艺复杂、产品差异性大的企业,可以考虑采用作业成本法,以实现更精细化的成本管理;而对于生产过程相对简单、产品结构相对单一的企业,则传统成本法可能更为适用,能够以较低的成本实现对整体成本的控制。

作业成本法和传统成本法各有其优势和适用场景,企业在选择成本计算方法时,应充分考虑自身特点和管理需求,以达到最佳的管理效果。

在不同情况下,作业成本法和传统成本法都有其独特的应用场景,企业应根据实际情况灵活选择,以实现成本控制和管理的最佳效果。

作业成本法和传统成本法的比较【摘要】:作业成本法与传统成本法既有区别又有联系,作业成本法从根本上解决了传统成本法的缺陷。

以作业为基础的成本计算是成本会计科学发展的大趋势, 在我国研究与推广作业成本法有着重大的理论与现实意义。

【关键词】:作业成本法;传统成本法一、作业成本法的产生及基本原理作业成本法(Activity Based Costing,简称ABC),是以作业为基础,通过对作业成本动因的分析来计算产品生产成本,并为企业作业管理提供更为相关、相对准确成本信息的一种成本计算方法。

作业成本法兴起于20世纪的美国,最早可以追溯到20世纪杰出的会计大师美国埃里克?科勒(Eric Kohler)。

科勒当时所面临的问题是,如何正确计算水力发电行业的成本。

在水力发电生产过程中,直接人工和直接材料(这里指水源)成本都很低廉,而间接费用所占的比重相对很高,这就从根本上冲击了传统成本核算方法一个基本前提,即:直接成本在总成本中所占的比重很高(工业革命以来,机器大生产中大量的劳动力投入和原料消耗一直是成本的主体)。

科勒由此提出了作业成本法的基本思想。

随着时间的推移,计算机为主导的生产自动化、智能化程度日益提高,各个生产领域中直接人工费用逐渐减少,间接成本逐渐增加。

传统成本法中”直接成本比例较大”的假定所收到的挑战越来越大。

在新的环境里,传统成本法中按照人工工时、工作量等分配间接成本的思路,严重扭曲了成本,无法为企业管理提供有效的信息。

在这一背景下,作业成本法逐渐兴起和完善,并率先在技术条件优良的制造业开始应用,在一定范围内取得了良好的效果。

作业成本法认为,传统的成本计算方法以产品作为成本分配的对象,把单位产品耗用某种资源(如工时)占当期该类资源消耗总额的比例,当成了对所有的间接费用进行分配的比例,是不合理的;成本分配的对象应该是作业,分配的依据应该是”作业”的耗用数量,即对每种作业都单独计算其分配率,从而把该作业的成本分配到每一种产品。

作业成本法与传统成本法的比较一.作业成本法与传统成本法的概念及比较(一)作业成本法与传统成本法的概念1.作业成本法的概念所谓作业成本法( Activit y- based costing, ABC 法) , 即以作业( activity) 为核心, 确认和计量耗用企业资源的所有作业, 将耗用的资源成本准确地计入作业, 然后选择成本动因, 将所有作业成本分配给成本计算对象( 产品或服务) 的一种成本计算方法。

2. 传统成本法的概念传统成本法指企业支持成本分摊的方法,支持成本指支持产品或服务完成的除直接材料、直接人工之外的成本费用。

传统成本计算方法的基本原理概括为:根据不同的成本计算对象归集生产过程中所发生的费用(二)作业成本法与传统成本法的比较在传统成本法下,间接费用为制造成本,就经济内容来看,只包括与生产产品直接、间接有关的费用,而用于管理和组织全厂生产、销售产品和筹集生产资金的支出作为期间费用。

在作业成本法下,产品成本则是完全成本,所有费用只要合理有效,都是对最终企业价值有益的支出,都该计入生产成本。

它强调的是费用支出的合理有效,而不论其是否与生产直接、间接有关。

在这种情况下,期间费用归集的是所有不合理的、无效的支出。

传统成本法计算成本的主要目的是把辅助部门归集的制造费用以一种平均线性方式的分配到各产品,没有考虑实际生产中产品消耗与费用的配比问题,只能是一种“绝对不准确”(absolute inaccu2racy)的信息。

作业成本法计算出的产品成本信息可视为一种相对准确(relative accuracy)的信息。

作业成本法分配间接费用时着眼于费用、成本的来源,将间接费用的分配与产生这些费用的原因联系起来。

在分配间接费用时,选择多样化的分配标准(成本动因),使成本的可归属性大大提高,并将按人为标准分配间接费用的比重降到最低限度,提高了成本信息的准确性。

如果把产品的成本视为靶心,作业成本法虽然不能每次都击中这靶心,但是却能始终如一地击中靶的外环和中环。

![作业成本法在制造业中的运用及利弊[外文翻译]](https://img.taocdn.com/s1/m/4b5fe230a417866fb84a8ebd.png)

外文翻译Utilization of Activity-Based Costing System in Manufacturing Industries – Methodology, Benefits and Limitations Material Source: International Review of Business Research PapersAuthor: Boris Popshop IntroductionThe difficulty inherent in choosing a proper and accurate product costing method for manufacturing enterprises has been widely discussed by academics and practitioners. The important limitation of traditional (absorption) costing methods had been deeply discussed along with advantages of other costing method as Variable Costing or Activity-Based Costing (ABC). Despite the fact that issues relating to ABC have been widely discussed by researchers and practitioners in the past ten years, this modern concept still lacks general rules governing both methodology and cost allocation principles. Looking back, the concept of Activity-Based Costing has been considered a sophisticated method of cost calculation since the early 1980s. The ABC method was originally designed as a solution to the limitations of traditional costing methods. The problems relating to these traditional costing methods had been discussed with the need for improvement in the quality of costing systems actually utilized in practice. However, one challenge faced when carrying out the cost allocation procedure in ABC lies in the manner in which the methodology is applied. When allocating costs in adherence to ABC principles, the user of the system also has to strictly follow the individual steps within the implementation methodology, where clearly defined allocation procedures and other methodical acts are performed. This research study has no ambitions to judge the expediency of the ABC system for recent or future users. In fact, the aim of this paper is to definitively explain the necessary steps to apply ABC, as well as to clarify procedures for activity output measurement and cost assignment. The paper also describes the benefits and limitation of ABC implementation in manufacturing industries.1. Literature review1.1 The ABC concept was designed as a method which eliminates the shortages of the traditionally used absorption costing methods. Traditional costing techniqueswere used for the purposes of overhead cost allocation during the 20th century. These are based on simplified procedures using principles of averages. In recent decades, such conventional concepts have become obsolete due to two major phenomena. The first of these is ever increasing competition in the marketplace, the necessity to reduce costs and the effect of having more detailed information on company costs. Secondly, there has been a change in the cost structure of companies. In terms of the majority of overhead costs, traditional allocation concepts, based as they are on overhead absorption rates, can often provide incorrect information on product costs. Those shortages or limitations had been very closely described in the scientific publications (Drury, 2001), (Lucas, 1997). The first criticism of traditional costing concept was published by Kaplan and Johnson in (1987).The effect that plays a role in determining an inaccurate overhead cost allocation could be described (figure 1) as ‘verbalization’ (Popshop, 2008). In other words, the end results of allocating a proportionally average volume of costs of any type to all cost objects. For example, the cost for transporting an item to customer A is the true value of 50€, and transport to customer B is 900€. If we use traditional absorption costing, the transport costs will become part of the sales or distribution overhead, meaning all the costs of this type will be mixed together and then allocated through the absorption rate to the cost object, in proportion to the specific type of direct cost. All cost objects then will be subject to the principal average volume of transport costs. In the example this means 130€ for customer A and 110€ for customer B. Above mentioned problems could be sometimes be solved by application of differentiation absorption costing, which uses several types of overhead with different allocation bases, instead of summing absorption costing with one universal overhead and one allocation base (Karl, 2006). Another possible solution is the application of cons centre overhead rates instead of planed-wide rate (Drury, 2001). Despite that, the p roblem of what here is termed ‘verbalization’ is also significant in companies with a very sophisticated system featuring cost centre overhead rates. Even if severalDifferent overhead rates for different overhead cost pools are used to improve the quality of cost assignment; the basis is still the same – the allocation base usually represented by any type of direct cost. If the basis is only set to the easily measured amount of direct costs, it is not possible to achieve accuracy in cost assignment, because the true causes of cost consumption frequently have a natural base. The absorption costing method could distort product costs because it allocates overheadcosts proportionally to the portion of direct costs. Glad and Becker (1996) identified a number of fundamental limitations in traditional costing systems:•Labor, as a basis for assigning manufacturing overhead, is irrelevant as it is significantly less than an overhead and many overheads do not bear any relationship to labor costs of labor hours•The cost of technology is not assigned to products based on usage. Moreover, direct (labor) cost is replaced by indirect (machine) cost(s)•Service-related costs have increased considerably in the last few decades. Costing for these services was previously non-existent•Customer-related costs (finance, discounts, distribution, sales, after-sales service, etc.) Are not related to the product’s cost objects Customer profitability has become as crucial as product profitabilityIn some instances, especially when a company has a very homogenous output, few departments with overheads and customers are very similar in nature, the simple absorption costing method should provide very accurate outputs, despite its limitations (Stank, 2003). The absorption costing method boasts one very important advantage - it is very simple to put into utilization. All the information the user has to gather together can be found in accounting books or product material and labor sheets.Kim and Ballard (2002) defined the problems that can result from using traditional methods of overhead costing as:•Cost distortion hinders profitability analysis•Little management attention to activities or processes of employeesThe logical solution of registered disadvantages of traditional absorption costing systems was to develop a costing method which would be able to incorporate and utilize cause-and-effect instead of widely applied arbitrary allocation principles into the company costing system (Drury, 2001), (Lucas, 1997). In situation, when the portion of overheads exceeds 50% of total company costs and the company is using single measures for allocation of overhead costs to the cost objects, the risk of an incorrect product or customer costs calculation becomes significant.Following the 1970s, there was a general realization of the limitations in traditional costing systems. Greater competition and further inaccuracies in costing products effectively encouraged businesses to seek out alternative methods, ones offering far more transparency and enabling accurate and causal cost allocation. Itwas then, at the dawn of the 1980s that the Activity-Based Costing (ABC) method came about, being quickly adopted by enterprises of many and various types. The spread of ABC owed a significant debt to advances in computing and IT thereby permitting practical utilization of ABC principles.The Activity-Based Costing method is a tool which could bring about significant improvement in the quality of overhead cost allocation. The ABC process is able to incorporate both physical measures and causal principles in the costing system. The basic idea of ABC is to allocate costs to operations through the various activities in place that can be measured by cost drivers. In other words, cost units are assigned to individual activities, e.g. planning, packing, and quality control using a resource cost driver at an initial stage with the costs of these activities being allocated to specific products or cost objects in a second phase of allocation via an activity cost driver.Activity-Based Costing methodology has been described, and further evolved, by many authors (Drury 2001), (Glad and Becker, 1996), (Kaplan and Cooper, 1998), (Stank, 2003). The ABC process could vary from simple ABC, using only one level of activities to expanded ABC, comprising various levels of activities and allowing for mutual allocation of activity costs (Cookies, 2001).Nevertheless, it should be noted that the ABC approach is not a truly revolutionary or a completely new means of allocation. In essence, it has transformed the logical relationships between costs and company outputs entering a costing system. Indeed, ABC has incorporated logical allocation procedures from costing systems predating its own complex methodology.1.2 Implementation methodologyTogether with the emergence of ABC methodology, issues relating to its practical utilization and implementation have been presented by both academics and practitioners. At this point, it is necessary to distinguish between two diverging approaches addressing ABC system implementation. The first considers implementation merely in terms of performing an ABC calculation and is primarily focused on the system’s construction, cost flow, and allocation procedures. Drury (2001) defined the necessary steps to set up an ABC system as follows:1. Identifying the major activities taking place in an organization2. Assigning costs to cost pools/cost centers for each activity3. Determining the cost driver for every activity4. Assigning the costs of activities to products according to their individualDemands on activitiesThese are described by other authors in a very similar manner. For example, Stank (2003), considers adjusting accounting input data as the initial procedure in building the system. Furthermore, he prescribes the fourth step of implementation as calculating the activity rate, which is defined as an activity unit cost.The above-defined steps of system design could be considered as a very brief overview for successful implementation process. Some other authors define much more detailed application procedures. The steps in the ABC application methodology defined by Glad and Becker (1996) are:1. Determine the nature of costs and analyze them as direct traceable costs, activity traceable costs and non-traceable costs (or unallocated costs)2. Account for all traceable costs per activity, distinguishing between primary and secondary activities3. Identify the company’s processes, activities and tasks, and create process flowcharts4. Determine cost drivers for each activity and use output measures to calculate activity recovery rates5. Trace all secondary activities to primary activities, so that the combined activity rates include all support costs6. Identify which cost objects are to be priced. Compile the bill of activities for each cost object7. Multiply the activity recovery rates by the quantity of output consumed as specified in the bill of activities. The sum of these calculated costs will give the activity-traced cost of the cost object8. Direct costs and non-traceable costs should be added to the cost calculatedAbove to give the total cost of the cost object the other approach to ABC implantation not only encompasses the structure, design of the system, and tackles the question of how costs are allocated in ABC, but also deals with issues related to its implementation within an organization. In other words, the question of how the ABC system must operate within an enterprise. This approach considers all the necessary features that have to be addressed in the process of setting up an ABC system. Many authors have described implementation in great detail (Coins, 2001), (Glad and Becker, 1996), (Innes and Mitchell, 1998). The procedures they analyze are far wider ranging than the steps involved in system design because of the focus on organizational, personnel, capacity, and affectivity issues of ABC systembuilding and utilization. Probably the most important matter solved by this approach to ABC application, which analyzes performance during its set-up, is the question of the efficacy of the future system. ABC usually processes large quantities of financial and non-financial data. If we want to maintain the effectiveness of the system, it is necessary to ensure that costs for obtaining that kind of the data do not outweigh the benefits of the system. Should this not be possible, the application of the system is ineffective? Applying ABC brings different benefits for different organizations. According to the characteristics of the system, we can say that putting the system in place would be effective in organizations with a complex and heterogeneous structure of activities, products, and customers.译文作业成本法在制造业中的运用及利弊资料来源:International Review of Business Research Papers作者:Boris Popshop 在为制造业企业选择合适、准确的成本核算方法的困难已被学者和实践者广泛的讨论。

作业成本法和传统成本法的比较研究以某大型机械加工企业为例一、本文概述在当今复杂多变的商业环境中,准确的成本信息对于企业的决策至关重要。

作业成本法(ActivityBased Costing, ABC)和传统成本法(Traditional Costing)是两种主要的成本计算方法。

本文旨在比较这两种方法在某大型机械加工企业的应用效果,以期为企业在成本管理方面提供参考。

本文将介绍作业成本法和传统成本法的基本原理和计算方法。

作业成本法通过将成本分配到各个作业活动中,更准确地反映了产品或服务的成本构成。

而传统成本法则通常采用简单的成本分配标准,如直接劳动小时或机器小时。

本文将分析在某大型机械加工企业中,这两种成本法是如何被应用的。

通过实际案例分析,本文将探讨作业成本法和传统成本法在该企业的具体实施过程,以及它们在成本分配、产品定价、利润分析和决策支持等方面的表现。

本文将基于比较分析的结果,提出针对该企业的建议。

这些建议将帮助企业更好地理解和使用作业成本法和传统成本法,从而优化成本管理,提高企业的竞争力和盈利能力。

本文通过比较研究,旨在深入理解作业成本法和传统成本法在某大型机械加工企业的实际应用,以期为相关领域的研究和实践提供有价值的见解。

二、作业成本法概述作业成本法(ActivityBased Costing,简称ABC)是一种成本核算和管理方法,它通过识别企业的各种活动并计算这些活动消耗资源的成本,进而将成本更准确地分配到产品或服务上。

与传统成本法相比,作业成本法的核心优势在于其能够提供更为精确和细致的成本信息,帮助企业更好地理解成本结构,从而做出更加合理的决策。

在大型机械加工企业中,作业成本法的应用尤为重要。

这类企业通常具有复杂的生产流程和多样化的产品线,传统的成本核算方法往往难以准确反映各个产品的实际成本。

通过实施作业成本法,企业可以将生产过程中的各种活动(如材料采购、加工、装配、检验等)识别并分类,然后根据每种活动的实际资源消耗来计算成本。

作业成本法在我国制造企业中的应用摘要作业成本法(Activity-Based Costing,简称ABC),是一种以作业为基础,通过对所有作业活动进行动态追踪,根据各项作业费用的消耗情况将成本进行合理分配的一种成本计算方法,它是对传统成本计算方法的创新。

不仅仅可以弥补传统成本管理的缺陷,而且为企业的生产经营管理提供及时,准确,相关的成本信息的计算方法。

随着对作业成本的不断研究,它首先在制造业中开始运用,并取得了理想的效果。

让研究人员看到,作业成本法可以改变传统成本核算方法的不足,且还能为企业成本管理提供很好的核算基础。

关键词:作业成本法;核算方法;效益AbstractCosting (Activity-Based Costing, referred to as ABC), is a kind of job basis, through the dynamic tracking of all work activities, in accordance with the operating costs of consumption will be a costing methodology reasonable cost allocation, it is the traditional costing methods innovation. You can not just make up the deficiencies of traditional cost management, and to provide timely, accurate and relevant information on the cost calculation method for production and operations management. With the study of operating costs, which first began to use in the manufacturing sector, and achieved the desired results. Allow researchers to see, you can change Costing less than traditional cost accounting methods, and also provides a good basis for the accounting cost management.Keywords: Costing; accounting methods; Benefit1.1、作业成本在我国制造企业中的背景1.2、作业成本在我国制造业企业中目的和意义;2、作业成本法的基本理论。

作业成本法与传统成本计算法之比较【摘要】文章对作业成本计算法的产生背景、理论依据及其与传统的制造费用分配方法的差异进行了比较与分析,有助于更深刻地了解作业成本计算法的优越性,以促进它在我国的推广与应用。

【关键词】作业成本法;成本计算法;优越性一、引言成本管理是企业管理的一个重要方面,提供准确的会计信息资料,有利于企业各项改革措施协调一致、齐头并进地推动各项企业管理朝着科学方向发展。

作业成本计算法即Activity-based Costing(ABC)是指以作业为核算对象,通过成本动因来确认和计量作业量为基础分配间接费用的一种成本计算方法。

其理论基础是:产品消耗作业,作业消耗资源并导致成本的发生。

作业成本计算法在成本计算方法上突破了传统方法的束缚,使成本核算深入到作业层面。

它以作业为单位归集成本,并把作业的成本按动因分配到产品。

20世纪70年代以来,许多企业采用了高度自动化的生产技术,以满足客户多样化、小批量,并能快速、高质量地生产出个性化强、品种多、批量小的产品。

随着自动化技术的产生与发展,生产状态由“多人操作一台机器”转变为“一人操作多台机器”。

因而,固定制造费用占有的产品制造成本比例大幅度上升。

在这种情况下,要求企业管理者对制造费用的核算作革命性变革,要求把成本核算的重点从直接人工转移到制造费用的合理分配上,以便提高产品成本计算的正确性和提高成本控制的有效性。

相对于传统成本计算法,作业成本计算法在理论上有本质的突破:作业成本计算法的理论基础可以表述为“作业消耗资源,产品消耗作业”。

资源是成本的源泉,包括人工、材料、生产维持成本,以及生产过程以外的成本,譬如广告费等。

资源按一定相关性进入作业,作业是协同生产中的工作的各个单位。

例如售后服务部门,其作业包括受理客户投诉意见、解决产品问题,以及反馈产品信息等三项作业。

作业可以看作是连接产品与资源的纽带,不仅产品成本是最终的成本计算对象,处于“中介”地位的作业也应成为成本计算对象。

作业成本法和传统成本计算方法的比较作为企业管理者,了解和掌握成本计算方法对于企业的经营和决策有着重要的意义。

传统的成本计算方法在长期以来一直被广泛应用,但是随着时代的发展和经济环境的变化,人们对于成本计算方法的要求也在不断提高。

在这种背景下,作业成本法作为一种新兴的成本计算方法逐渐得到人们的关注和应用。

本文旨在浅谈作业成本法和传统成本计算方法的比较,探讨其优缺点和适用场景。

作业成本法是一种以作业为单位进行成本计算的方法。

作业可以理解为生产过程中的一个环节,可以是一项产品的生产过程,也可以是一项服务的提供过程。

作业成本法通过对每个作业的直接和间接成本进行精确计算,实现对作业成本的准确和及时控制。

作业成本法强调的是作业的过程和成本的追踪,能够提供详细的成本信息,帮助企业更好地进行成本控制和决策。

与传统的成本计算方法相比,作业成本法在许多方面有着明显的优势。

首先,作业成本法更加适应现代企业的复杂性和多样性。

传统成本计算方法通常是基于全成本法,即将成本平均分配到产品或服务上,这样的方式在今天的企业环境下已经显得不太灵活和准确。

而作业成本法能够针对每个作业进行精确的成本计算,不仅可以更好地反映作业的真实成本,还可以帮助企业更好地了解每个作业的盈利能力。

其次,作业成本法提供了更准确和详细的成本信息。

作业成本法将一切费用和成本都与作业相关联,能够更清晰地展现出作业成本的构成和动态变化。

传统的成本计算方法往往只提供总成本的统计数据,无法直观地了解作业的细节和成本的构成。

而作业成本法可以提供每个作业的直接成本和间接成本,帮助企业更好地分析和管理成本,优化资源配置和利润。

此外,作业成本法还能够借助技术手段实现自动化和数字化管理。

随着信息技术的不断发展,作业成本法可以通过计算机系统来实现对作业成本的实时追踪和计算,减少人工操作的错误和成本。

相比之下,传统的成本计算方法需要更多的手工输入和计算,容易出现数据错误和延误。

作业成本法在制造企业中的应用研究作业成本法在制造企业中的应用研究一、引言作业成本法(Activity-based costing,简称ABC法)是一种管理会计方法,旨在帮助企业更准确地分配成本和了解经营活动的成本结构。

在制造企业中,成本控制和成本分析是非常重要的事项,它们直接影响企业的利润和竞争力。

本文将探讨ABC法在制造企业中的应用,旨在提升企业的成本管理效率和决策水平。

二、ABC法的基本原理ABC法是基于活动成本驱动原理,强调对企业活动的分析和测算。

传统的成本分配方法主要侧重于直接劳动力和直接材料的成本,忽略了其他间接成本的影响。

而ABC法通过将企业的间接成本与实际活动相关联,更准确地进行成本分配。

ABC法的基本步骤包括:识别活动、计算活动驱动因素、分配资源消耗、计算单个产品的成本和作出决策。

三、ABC法在制造企业的应用1. 活动成本识别在使用ABC法进行成本核算前,首先需要识别各种活动,并对其进行详细描述。

通常,制造企业的活动可以分为原材料采购、生产准备、生产过程和产品交付等环节。

通过准确识别和描述活动,可以使成本分析更具针对性,发现影响成本的主要因素。

2. 活动驱动因素的计算活动驱动因素是指影响活动产生成本的各种因素,如工时、零部件数量、机器使用小时等。

在ABC法中,通过计算活动驱动因素,可以将各项成本准确分配给相关活动。

例如,对于生产准备活动,驱动因素可以是生产计划的变更次数、产品的种类或规格等。

3. 资源消耗的分配ABC法不仅考虑了直接成本,还将间接成本与活动相关联,进一步分解成本的组成部分。

例如,制造企业的间接成本可以包括设备折旧费、管理人员工资、设备维护费等。

通过将这些间接成本与活动的驱动因素进行关联,可以更准确地计算每个活动的资源消耗。

4. 产品成本计算ABC法的核心是将成本准确地分配给各个成本对象,如产品或服务。

在制造企业中,通过将活动驱动因素和资源消耗与产品的生产过程相关联,可以计算出每个产品的成本。

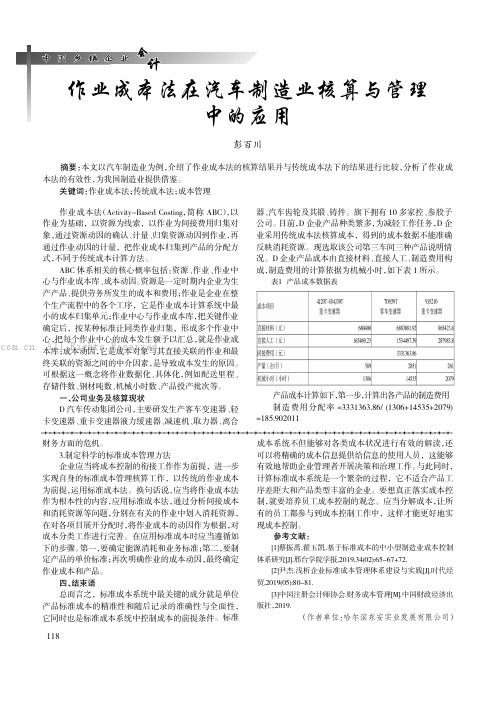

作业成本法在汽车制造业核算与管理中的应用彭百川摘要:本文以汽车制造业为例,介绍了作业成本法的核算结果并与传统成本法下的结果进行比较,分析了作业成本法的有效性,为我国制造业提供借鉴。

关键词:作业成本法;传统成本法;成本管理作业成本法(Activity-Based Costing,简称ABC ),以作业为基础,以资源为线索,以作业为间接费用归集对象,通过资源动因的确认、计量、归集资源动因到作业,再通过作业动因的计量,把作业成本归集到产品的分配方式,不同于传统成本计算方法。

ABC 体系相关的核心概率包括:资源、作业、作业中心与作业成本库、成本动因。

资源是一定时期内企业为生产产品、提供劳务所发生的成本和费用;作业是企业在整个生产流程中的各个工序,它是作业成本计算系统中最小的成本归集单元;作业中心与作业成本库,把关键作业确定后,按某种标准让同类作业归集,形成多个作业中心,把每个作业中心的成本发生额予以汇总,就是作业成本库;成本动因,它是成本对象与其直接关联的作业和最终关联的资源之间的中介因素,是导致成本发生的原因。

可根据这一概念将作业数据化、具体化,例如配送里程、存储件数、钢材吨数、机械小时数、产品投产批次等。

一、公司业务及核算现状D 汽车传动集团公司,主要研发生产客车变速器、轻卡变速器、重卡变速器液力缓速器、减速机、取力器、离合器、汽车齿轮及其锻、铸件。

旗下拥有10多家控、参股子公司。

目前,D 企业产品种类繁多,为减轻工作任务,D 企业采用传统成本法核算成本,得到的成本数据不能准确反映消耗资源。

现选取该公司第三车间三种产品说明情况。

D 企业产品成本由直接材料、直接人工、制造费用构成,制造费用的计算依据为机械小时,如下表1所示。

表1产品成本数据表产品成本计算如下,第一步,计算出各产品的制造费用制造费用分配率=3331363.86/(1306+14535+2079)=185.902011财务方面的危机。

3.制定科学的标准成本管理方法企业应当将成本控制的衔接工作作为前提,进一步实现自身的标准成本管理核算工作,以传统的作业成本为前提,运用标准成本法。

作业成本计算法与传统成本计算法的比较这里所说的传统成本计算法,实际上是指传统的间接成本分配法。

传统的间接成本分配法,是指以直接人工工时、直接人工成本、机器台时等作为分配基础,分配间接费用的一种成本计算方法。

按传统成本计算法,某产品的成本是由直接成本和间接成本两部分组成。

一般情况下,间接成本的计算公式是:某产品间接成本=该产品直接工时(或台时等)总数×间接费用分配率式中间接费用分配率的计算公式是:间接费用分配率=)(单位直接工时产量间接费用总额⨯∑ 在这种方法下,从总体看,生产的产品产量越多,决定间接成本费用分配率的公式中的分母就越大,从而使间接成本分配率就越小。

在间接费用总额和单位工时一定的情况下,产量越高,间接费用分配率就越低,单位产品成本就越低。

这就导致许多企业为降低单位产品成本而进行大批量的产品生产。

当增加的产品销售不出去或不能马上销售出去时,就会增加存货成本;当产品由于积压变质而报废时,其损失将远远大于由于增加产量而形成的产品成本节约额。

再从各种产品分别看,各种产品分摊的间接费用又与产量成正比,实际上,间接费用并不与产量成正比。

但是,这种分配方法在几十年前是合理的。

因为当时的大多数公司只生产少数几种产品,构成产品成本最重要的因素是直接人工成本和直接材料成本,且这两种成本占产品成本的很大部分,而制造费用的比重很小,因此,用少量的制造费用构成产品成本主体的直接人工去分配,所导致的扭曲是非常小的,产品成本信息是比较准确的。

然而,随着科学技术的快速发展,全球性竞争的加剧,公司及其生产环境发生了巨大的变化:生产成本中固定制造费用比重增大,直接人工比重下降,从而制造费用分配率很大,很容易造成产品成本失真;随着与工时无关费用的快速增加,用不具有因果关系的直接人工去分配这些费用,必定产生虚假的成本信息。

这些虚假的、失真的成本信息导致经营决策的失误、成本失控和降低财务报告的可靠性。

作业成本计算法正是以克服传统成本计算方法的弊端而产生的。

作业成本法与传统成本法的对比分析【中文摘要】作业成本法(Activity-based Costing Calculating简称ABC法)应时代的要求产生并发展,包括作业成本计算和作业管理。

本论文主要试从理论上对作业成本核算的准确性、作业成本管理的有效性两方面,运用比较分析法对作业成本法与传统成本法进行理论研究,同时对作业成本法加以实证分析,阐明ABC法应用的优越性。

【关键词】作业成本计算;作业分析法;传统成本法;应用对比研究【Summary】Activity-based costing (ABC) is a new subject in accounting field as well as in management accounting. ABC includes Activity-based costing calculating and Activity management. This thesis has proved that activity-based costing is an excellent cost method by theory and demonstration analysis, because ABC can provide accurate costing information, it can make cost management more effective.【Key words】Activity-based Costing Calculating; Activity Management; Traditional cost accounting methods;Application Research.一、作业成本法与传统成本法的发展历程产业革命的兴起使机器代替人工,工厂制代替手工工场, 产品制造程序日趋复杂,间接费用大量增加,同时这一时期,生产的自动化程度不高、需求较为单一,企业生产主要采用大批量少品种的生产方式,人力资源约占产品成本的40 %~50 % ,制造费用约占产品成本的10 %。

作业本钱法与传统本钱法的比拟及应用分析作业本钱法与传统本钱法的比拟及应用分析摘要本文主要阐述作业本钱法与传统本钱法的根本原理,应用比拟分析法,得出在我国企业实施作业本钱法的必要性及可行性,并简要分析目前我国企业实施作业本钱法现状进而提出相应的改良措施。

关键词作业本钱法传统本钱法比拟应用中图分类号:F275.3 文献标识码:A1传统本钱法概述传统本钱法产生于上世纪初,当时大规模、单一品种的生产特点使传统本钱核算方法在本钱核算中发挥着举足轻重的作用。

传统本钱计算方法的根本原理可以概括为:直接材料直接计入,间接费用分配计入的原那么。

直接材料是指产品生产过程中消耗的直接原材料和直接人工的本钱之和,间接费用仅包括生产过程中的制造费用和与产品生产直接相关的辅助费用,除此之外外表非相关费用统一归为期间费用,并不计入产品的本钱中去。

2作业本钱法概述作业本钱法,保存了传统本钱核算方法中的直接材料直接计入的环节,之后从整个产品的生产过程出发,分析产品价值链的各个环节,选择不同的作业作为本钱归集的本钱库,根据这些作业合理选择作业本钱动因,计算作业本钱动因率将本钱分配到不同的作业对象,最终计算出产品本钱。

其核心是:产品消耗作业,作业消耗资源。

通过作业的划分,更好地区分增值作业与非增值作业,进而通过增加高效增值作业产品的本钱,降低增值作业低效率产生的本钱和非增值作业产生的本钱。

作业本钱法不仅满足管理者对本钱核算准确度的要求,而且便于部门间的业绩考核。

3作业本钱法与传统本钱法的比拟作业本钱法作为更加合理、准确的本钱分配方法,它继承了传统本钱法直接材料直接计入原那么的根底上,对制造费用和间接费用的分配采用作业的形式,突破了传统本钱法按工时分配间接费用的标准,使得财务人员不仅关注产品的生产过程,更加注重生产的前因后果。

因此,作业本钱法是一种更为科学的本钱分配方法。

然而,两种核算方法拥有许多不同和相似之处。

3.1本钱法与传统本钱法的区别3.1.1与之相适用的企业经营特点不同传统本钱核算方式下的企业产品结构比拟单一、直接材料和直接制造费用占企业总本钱绝大局部且居于长期稳定的水平,使得传统本钱方法足以满足管理者对本钱简单核算的需求。

作业成本法与传统成本法比较作者:佟建立来源:《现代经济信息》2011年第01期摘要:与传统成本法相比,作业成本法适应“小批量、多品种”的现代化柔性生产方式成本核算要求,解决了传统成本核算在新制造环境下出现的种种问题,本文拟通过比较两种方法的差异,展示这种革新性成本核算方法的优越性所在。

关键词:作业成本法;传统成本法;比较中图分类号:F275.3文献标识码:A文章编号:1001-828X(2011)01-0059-01一、作业成本法(Activity basecosting)介绍20世纪30年来,基于对水力发电活动成本核算研究,美国经济学家科勒(Kohler)首次将作业观念引入会计管理中,是为作业成本法萌牙。

斯拖布斯(G.T.Staubus)在20世纪中期至80年代在其著作《收益的会计概念》、《作业成本计算和投入产出会计》、《服务与决策的作业成本计算——决策有用框架中的成本会计》提出一系列作业成本观念,为作业成本法的发展起到十分重要的作用。

20世纪末,美国芝加哥大学教授库珀(Robin Coopre)的《ABC四论》和作业成本法的集大成者哈佛大学教授卡普莱(Robert s.Kaplan)《管理会计相关性消失》标志着作业成本的全面兴起。

作业成本法主要着眼于通过于企业价值链的分析研究,确定作业动因,从而合理分配间接成本,作业成本法不但改变了基于数量的间接费用分配方式,也通过从采购到销售整个价值链资源及作业分析拓展间接费用范畴,完成了成本核算从“绝对不准确信息”到“相对准确信息”的转变,提高产品成本计算的正确性和提高成本控制的有效性。

作业成本法认为作业消耗资源,而产品则消耗了作业,因此,作业成本法涉及两个阶段的间接费用分配过程,第一阶段,根据资源动因把有关生产或服务的间接费用归集为作业中心,形成作业成本;第二阶段,通过作业动因把作业成本库归集的成本分配到产品或服务中去,最终形成产品或服务成本。

在作业成本法下,作业成本可分为四个层次的产品单位成本。

摘要随着我国经济的发展和市场的成熟,竞争愈发激烈,企业要想获得和保持持久竞争优势,成本信息的有效性和相关性不可忽视。

而成本核算是企业获得成本信息最重要的手段,因此,成本核算方法的选择非常重要。

下面就我国目前采用的制造成本法与西方广泛采用的作业成本法进行比较和分析。

关键词:制造成本法,作业成本法,异同;AbstractWith the development of our national economy and the maturity of the market, the increasingly fierce competition, the enterprise wants to obtain and maintain a lasting competitive advantage, cost effectiveness and relevance of information can not be ignored. And cost accounting is the enterprise obtains the cost information of the most important means, therefore, the cost accounting method of choice is very important. Below with respect to our country current adopted manufacturing costing and activity-based costing method widely used by western countries are compared and analyzed.Key words: manufacturing cost method, activity-based costing, similarities and differences;目录摘要 (1)Abstract (1)目录 (1)一、制造成本法的核算特点 (2)1.1.核算内容 (2)1.2.核算方法 (2)1.3.核算过程 (3)二、制造成本法成本核算的弊端 (3)2.1.制造费用的核算 (3)2.2.期间费用的核算 (4)2.3.人工费用的核算............................................................................... 错误!未定义书签。

作业成本法在制造业中的深度应用在深入探究作业成本法(ActivityBased Costing, ABC)在制造业中的应用之前,我先来回顾一下作业成本法的基本原理。

作业成本法是一种成本计算方法,它通过将企业的全部成本分为直接成本和间接成本,再根据成本动因(如生产订单、机器小时、人工工时等)将间接成本分配到各个成本对象上,从而更加精确地追踪和分配成本。

一、作业成本法在制造业中的应用过程1. 成本归集与分析在制造业中,生产一个产品需要经过多个部门和环节的合作。

传统的成本计算方法往往无法准确反映各个环节的成本状况。

通过运用作业成本法,我们可以将生产过程中的各项成本按照成本动因归集到各个作业环节中,从而深入了解每个环节的成本结构和成本效益。

2. 作业动因的确定与分析作业成本法的核心在于确定成本动因,并将间接成本分配到各个成本对象上。

在制造业中,成本动因的确定需要综合考虑多种因素,如生产订单、机器小时、人工工时等。

通过对成本动因的分析,我们可以找出影响成本的关键因素,从而为成本控制和优化生产流程提供依据。

3. 优化生产流程作业成本法可以帮助企业发现生产过程中的浪费和低效环节。

通过对成本数据的深入分析,企业可以找出关键的成本动因,进而优化生产流程、提高生产效率。

例如,某企业通过作业成本法发现,生产某一产品的人工成本较高,原因是该产品的生产过程中存在过多的手工操作。

企业于是对生产流程进行改进,引入自动化设备,从而降低了人工成本,提高了生产效率。

4. 定价策略制定作业成本法为企业提供了更加精确的成本信息,有助于制定合理的定价策略。

通过对各个成本对象的盈利能力进行分析,企业可以更加科学地确定产品价格,提高盈利水平。

例如,某企业通过作业成本法发现,其某一产品的成本结构发生了变化,成本较高的原因是原材料采购价格上升。

企业于是调整了采购策略,降低了原材料成本,从而提高了产品竞争力。

5. 成本控制与绩效评价作业成本法为企业提供了一种有效的成本控制和绩效评价方法。

外文文献翻译原文:Application of Activity-Based Costing in aManufacturing Company: A Comparison withTraditional CostingAbstractActivity-Based Costing (ABC) represents an alternative paradigm to traditional cost accounting system and has received extensive attention during the past decade. Rather than distorting the cost information by using traditional overhead allocation methods, it traces the cost via activities performed on the cost objects (production or service activities) giving more accurate and traceable cost information. In this paper, the implementation of ABC in a manufacturing system is presented, and a comparison with the traditional cost based system in terms of the effects on the product costs is carried out to highlight the difference between two costing methodologies. The results of the application reveal the weak points of traditional costing methods and an S-Curve which exposes the undercosted and overcosted products is used to improve the product pricing policy of the firm.1. IntroductionTh e customer driven environment of today’s manufacturing systems and the competitive pressure of the global economy force manufacturing services and organizations to become more flexible, integrated and highly automated in order to increase their productivity at reduced costs. But it is impossible to sustain competitiveness without an accurate cost calculation mechanism [1]. Proposed by [2], as an alternative method to traditional cost accounting methods, ABC assigns costs to activities using multiple cost drivers, then allocates costs to products based on each product’s use of these activities [3], [4]. Using multiple activities as cost drivers, it reduces the risk of distortion and provides accurate cost information [3].In an ABC system, the total cost of a product equals the cost of the raw materialsplus the sum of the cost of all value adding activities to produce it [4]. In other words, the ABC method models the usage of the organization resources by the activities performed and links the cost of these activities to outputs, such as products, customers, and services [5]. Each product requires a number of activities such as design, engineering, purchasing, production and quality control. Each activity consumes resources of different categories such as the working time of the manager. Cost drivers are often measures of the activities performed such as number of units produced, labor hours, hours of equipment time, number of orders received.In traditional cost accounting systems, direct materials and labor are the only costs that can be traced directly to the product. By using the ABC system, activities can be classified as value-added and non-value-added activities. In order to improve the performance of the system, non-value-added can be eliminated.Despite the advantages of providing accurate costs, it requires additional effort and expense in obtaining the information needed for the analysis [6]. However, a proper design tool can help to reduce time used for modeling and overcome the difficulties present in designing a cost model.The primary objective of this paper is to develop an ABC system for a sanitary-ware company and to compare the results of ABC with traditional costing methods. In other words, the aim of ABC analysis is to guide improvement efforts of management in the right direction by providing accurate information about activities. The organization of the paper is as follows: In section 2, the methodology of ABC is explained. A case study is presented in section 3 to illustrate the application of ABC in a company. Finally, in section 4, the conclusions and the future research directions are given. Some suggestions are offered to improve the performance of the company.2. Activity-Based Costing (ABC)ABC is an economic model that identifies the cost pools or activity centers in an organization and assigns costs to cost drivers based on the number of each activity used. Since the cost drivers are related to the activities, they occur on several levels: 1. Unit level drivers which assume the increase of the inputs for every unit that isbeing produced.2. Batch level drivers which assume the variation of the inputs for every batch that isbeing produced.3. Product level drivers which assume the necessity of the inputs to support theproduction of each different type of product.4. Facility level drivers are the drivers which are related to the facility’smanufacturing process. Users of the ABC system will need to identify the activities which generate cost and then match the activities to the level bases used to assign costs to the products.While using the ABC system, the activities which generate cost must be determined and then should be matched to the level drivers used to assign costs to the products. The implementation of the ABC system has the following steps:1. Identifying the activities such as engineering, machining, inspectionetc.2. Determining the activity costs3. Determining the cost drivers such as machining hours, number of setups andengineering hours.4. Collecting the activity data5. Computing the product cost3. Implementation of the ABC Method: A Case StudyThe implementation study presented here took place in one of the leading sanitaryware companies in Turkey [7]. It has a production capacity of 6.8 thousand tons. Like many sanitaryware manufacturers, the company includes some common processes. First stage of the processes is done in the bulk-preparement department which is in charge of preparing the essential quantities of bulk bearing. Recipes are prepared for each production run and according to this ingredient recipes, the bulks are prepared by the electronically controlled tanks. After the bulk is ready, it can be sent to two different departments, pressured and classical casting departments.In pressured casting department, the bulk is given shape by the pressured casting process. The process uses automated machines and has shorter cycle times when compared to classical casting department. However, the bulk used in this department must have the characteristics of strength and endurance. The output of this departmentis sent to glazing department.Classical casting is the second alternative to produce sanitaryware products. In this department, most of the operations are performed by direct labor. The cycle times of the products are longer than the pressured casting department. The output of this department is“shaped and casted” bulk and sent to the glazing department, too.In glazing department, shaped bulk is glazed. This stage can be defined as polishing the products with a protective material from external effects. The output of this department is sent to tunnel oven. In tunnel oven, the products are heated over 1200 degrees Celsius. After staying in theses ovens for a period of time, the products are inspected by the workers. However, some of the output may have some undesired characteristics like the scratches, etc. In this case, these products are sent to the second heat treatment where they are reworked and heated again. The proper output is sent to packaging while the defected ones are sent to waste. Finally, in packaging department, products are packaged and shrunken. Company has been using a process costing logic for obtaining the proper costing of its products. Process costing is also a widely used costing tool for many companies. This method recognizes the following cost pools:– Direct Labor: All workers taking place in the production are recognized as direct labor and this pool is the most common pool used in every stage.–LPG-Electricity hot water: These items are important costing element in casting departments.– Packaging: This cost is observed in the final stage of the firm called final packaging. It includes packaging and shrinking of the products.– Overheads: This is also common cost pool for all the stages in the firm. It includes depreciation, rents, indirect labor, materials, and miscellaneous costs.In order to perform ABC calculations, process costing sheets are used. Because process costing aggregates the cost in the case of more than one product, it is difficult to obtain the correct results. The correct results with process costing can only be achieved when there is a single homogenous product. After analyzing the output of bulk preparement department, it is seen that bulk prepared for the two departments arethe same which brings an opportunity for the analysis.Firstly, time sheets are prepared to learn how much of the labor time is used to perform the relevant activities. Workers filled the time sheet and as a result, the activity knowledge of the processes and related percentage times are obtained. The time sheets are edited and necessary corrections are made. While some of the activities are merged, some of them are discarded. After this stage, the wage data is requested from the accounting department and labor cost of the activities are determined.If the amount of the activities that each product consumes can be learnt, the product costing can be calculated by taking the sum of the costs of the activities consumed by these products. Observations and necessary examinations are done to reach this knowledge and the conversion costs are loaded onto the activities. Cost of rent is loaded according to the space required for each activity and similarly, the power, depreciation and other conversion costs are loaded on the activities according to the activities’ consumption of the resources. If activity a uses 2/5 and activity b covers 1/5, while activity c covers 2/5 of the department space, then activity a is given 2/5, b is given 1/5 and c is given 2/5 of rent. All the conversion costs are distributed by using the same logic. The activities performed during classical casting are: molding, drilling assembly holes, rework, equipment clean-up, drilling function holes and carrying. The activity driver for molding is the processing time, for drilling assembly holes is the number of holes, for rework is the number of outputs, for equipment clean up is the total processing time, for drilling function holes is the total number of function holes and for carrying are the number of processed units in this department, unit area the product allocates on the carrier and the total area of carried goods.The activities performed during pressured casting are: molding, drilling lateral holes, setup, cutting excess materials from the products, general rework, carrying WIP, drilling assembly holes, ring preparation, drilling some subcomponents washbasins, washbasin drilling, rework of back of the products, X-patch control, bringing the WIP, helping to other departments, filling forms, mold check-up, WIP control, equipment and personnel control, drilling water holes. The activity driver for molding is thenumber molds used, for drilling lateral holes is the number of output, for setup are the incoming units, setup hour, setup for other products, setup for basins, setup for other products, for cutting excess materials from the products is the incoming units, for general rework is also the incoming units, for carrying WIP is the number of output, for drilling assembly hole and for ring preparation is the number of output, for drilling some sub-components washbasins is the number of subcomponents, for washbasin drilling is the number of washbasins, rework of back of the products and X-patch control is the number of output, for bringing the WIP is the incoming WIP, for helping to other departments is the number of reservoirs, for filling forms, mold check-up, WIP control, equipment and personnel control, drilling water holes is the incoming units.The activities performed during glazing are maintenance, glazing with hand, WIP transfer, rework, closet shaking, planning, routine controls and prism data entry. The activity driver for maintenance is the number of reworked parts, for glazing with hand is the weight of parts to be glazed, for WIP transfer and rework is the number of reworked parts, for closet shaking is the number of closets, for planning, routine controls and prism data entry is the planned units.The activities performed in the tunnel oven department are tunnel oven activity, transfer to oven, transfer from oven, heat control, oven security control, planning, routine controls, prism data entry, taking records, second heat treatment activity, WIP feeding to the oven, rework of heat processed units and special treatment. The activity driver for tunnel oven activity, transfer to oven, transfer from oven, heat control and oven security control is the total area covered by the heated units, for planning, routine controls, prism data entry and taking records is the total sum of outputs, for second heat treatment activity and WIP feeding to the oven is total area covered by all units, for rework of heat processed units and special treatment is the total area covered by outputs.The activities performed in the packaging department are packaging, shrinking, clean-up, organizing the finished products, maligning, and product function control and transferring the outputs. The activity driver for packaging and shrinking is thepackaged volume, for clean-up is the total number of units cleaned, for organizing the finished products, maligning, product function control and transferring the outputs is the total number of outputs.After finding the product costs of the firm, the costs obtained by process costing methodology and the ABC results of the product costs are compare From the results, it is seen that there are significant differences between some the product costs obtained by the two methods.4. ConclusionsABC utilizes the activity concept and by using the activities, ABC can successfully link the product costs to production knowledge. How a product is produced, how much time is needed to perform an activity and finally how much money is absorbed by performing this task are answered by the help of ABC studies.An S-Curve will exist after the comparison of the traditional and ABC costs [8]. The following notation is used for the comparison of the two product cost values. % Bias of ABC from traditional costing is found for each product. % bias = (ABC cost/traditional cost)*100.Product costs under ABC and traditional costing views can be used to design a table (Table 1) which illustrates %bias of ABC and traditional costs.Table 1. Comparison of the two product cost valuesNote that the table includes only the products that are sold. Products that are not sold but left as semi products are not involved.The results show 3 significant regions:1. Products undercoated by traditional costing:The costs of these products are higher than the“process-costing” and when plotted are greater than the value 100 at y axis. Before the ABC study was implemented, firm was not aware of this hidden loss of money for each of these products. By the help of the ABC study, people noticed this “hidden loss” and pricing decisions are examined.2. Products overcosted by the traditional methods:These products are the ones which have smaller values than the value 100 of y-axis. By the help of the ABC, firm realized that, the costs of these products are lower than the costs obtained by process costing. A “hidden profit zone” occurs for these products. Without any intention, a hidden benefit is gained from these products by traditional costing. But noticing the real ABC costs of these products, the firm can re-price these outputs and can gain a competitive advantage.3. Products which are costed almost the same:These are the products whose costs result nearly the same by using the two methods.A narrow band of 20 percentage (%80-%120) can be accepted for this region.Fig. 1. S-CurveFrom the ABC analysis, it is seen that while some of the products are undercosted, and overcosted, some of them give nearly the same results.In the analysis, the cost calculations of the bulk preparement department are performed using traditional costing method. When the outputs of the processes are identical or nearly identical, then ABC must be avoided to implement. Because ABC consumes lots of time, data and efforts, implementation of it has also a cost. For identical outputs, both ABC and traditional give the same results, so it is not logical to implement ABC.By the help of this analysis, product-pricing decisions gain importance. Pricing decisions can be done under the scope of these hidden losses and profits. According to the ABC results, the company will probably increase or decrease some of its product costs to gain more competitive advantage.The costing process of the company highlighted some weaknesses of the information system, too. These problems are also expected to be fixed in the future. As it is seen in this application, ABC is capable of monitoring the hidden losses and profits of the traditional costing methods. The existence of S-Curve shows which ones of the products are under or overcosted. As a further work, in thecompany, performance analysis are expected to be done and especially Balanced Score Card (BSC) implementations can be performed. The existence of the ABC database is an advantage for BSC applications since its financial phase recommends an ABC implementation. Kaizen applications and BSC can give the firm great advantages in the short and long run under the scope of ABC.The studies in literature promote that ABC is a promising method to support pricing, product mix, and make or buy decisions in manufacturing companies.ABC is a fruitful area for researchers and has high potential for novel applications such as the hybridization of ABC with meta-heuristics methods as Artificial Neural Networks, Genetic Algorithms, and Simulated Annealing.References1. Ozbayrak, M., Akgun, M., and Turker, A.K.: Activity-based cost estimation in a push/pull advanced manufacturing system. Int. J. of Production Economics, vol. 87 (2004) 49-65.2. Cooper, R. and Kaplan, R. S.: How cost accounting distorts product costs. Management Accounting, vol.69 (1988) 20-27.3. Kim, G., Park, C. S., and Kaiser, M. J.: Pricing investment and production activities for an advanced manufacturing system, Engineering Economist, vol. 42, no. 4 (1997) 303-324.4. Gunasekaran, A., and Sarhadi, M.: Implementation of activity-based costing in manufacturing. Int. J. of Production Economics, vol.56-57 (1998) 231-242.5. Ben-Arieh, D. and Qian L.: Activity-based cost management for design and development stage. Int. J. of Production Economics, vol.83 (2003) 169-183.6. Lewis, R. J.: Activity-based models for cost management systems. Quorum Books, West-port, CT (1995).7. Koker, U.: Activity-based costing: Implementation in a sanitaryware company. M.Sc. Thesis, Department of Industrial Engineering, University of Dokuz Eylul (2003).8. Cokins, G.: Activity-based cost management making it works. McGraw-Hill. Inc. (1997).Source: Gonca Tuncel, Derya Eren Akyol, Gunhan Mirac Bayhan, Utku Koker. Application of Activity-Based Costing in a Manufacturing Company: A Comparison with Traditional Costing[J].Lecture Notes in Computer Science, 2005, (16):562-569.一、翻译文章译文:作业成本法在一制造公司应用:与传统的成本核算比较1.简介客户驾驭着当今制造业系统的环境,全球经济的竞争压力迫使制造业的服务和组织需要变得更灵活、更完整,不断加强自动化,从而提升其生产力、降低成本。

作业成本法标准成本法产品成本法的关系

作业成本法(Job costing)、标准成本法(Standard costing)和产品成本法(Process costing)都是成本核算方法,用于确定和分

配生产成本。

它们之间的关系如下:

1. 作业成本法:适用于生产批量小、领域特定的产品或服务。

作业成本法将生产过程分解为不同的作业,为每个作业确定独立的成本。

这种方法通常适用于定制生产和个别订单生产情况,例如制造工

艺复杂的定制机械设备。

2. 标准成本法:标准成本法通过预先设定的标准成本,来评估

实际生产成本的合理性和效率。

标准成本法将产品的成本分为直接材

料成本、直接人工成本和制造费用,并为每个成本元素设定一个标准。

标准成本法适用于生产过程相对稳定且大量生产的情况下,例如大规

模的连续流程生产。

3. 产品成本法:产品成本法是一种综合了作业成本法和标准成

本法的方法。

它将生产过程分为不同的阶段或部门,并根据每个阶段

的实际成本和产量量化产品的成本。

产品成本法适用于生产过程中存

在多个阶段或部门,且每个阶段或部门的成本和产量可以量化的情况。

综上所述,作业成本法、标准成本法和产品成本法是根据生产特

点和需求选择的不同核算方法。

某些情况下,这些方法可能会结合使用,以更好地评估和控制生产成本。

外文翻译原文Application of Activity-Based Costing in a Manufacturing Company: A Comparisonwith Traditional CostingMaterial Source: Department of Industrial Engineering, University of Dokuz Eylul, TurkeyAuthor: Gonca Tuncel, Derya Eren Akyol, Gunhan Mirac Bayhan, Utku Koker Abstract: Activity-Based Costing (ABC) represents an alternative paradigm to traditional cost accounting system and has received extensive attention during the past decade. Rather than distorting the cost information by using traditional overhead allocation methods, it traces the cost via activities performed on the cost objects (production or service activities) giving more accurate and traceable cost information. In this paper, the implementation of ABC in a manufacturing system is presented, and a comparison with the traditional cost based system in terms of the effects on the product costs is carried out to highlight the difference between two costing methodologies. The results of the application reveal the weak points of traditional costing methods and an S-Curve which exposes the undercosted and overcosted products is used to improve the product pricing policy of the firm.1 IntroductionThe customer driven environment of today’s manufacturing systems an d the competitive pressure of the global economy force manufacturing services and organizations to become more flexible, integrated and highly automated in order to increase their productivity at reduced costs. But it is impossible to sustain competitiveness without an accurate cost calculation mechanism. Proposed by, as an alternative method to traditional cost accounting methods, ABC assigns costs to activities using multiple cost drivers, and then allocates costs to products based on each product’s use o f these activities. Using multiple activities as cost drivers, it reduces the risk of distortion and provides accurate cost information.In an ABC system, the total cost of a product equals the cost of the raw materials plus the sum of the cost of all value adding activities to produce it. In other words, the ABC method models the usage of the organization resources by theactivities performed and links the cost of these activities to outputs, such as products, customers, and services. Each product requires a number of activities such as design, engineering, purchasing, production and quality control. Each activity consumes resources of different categories such as the working time of the manager. Cost drivers are often measures of the activities performed such as number of units produced, labor hours, hours of equipment time, number of orders received.In traditional cost accounting systems, direct materials and labor are the only costs that can be traced directly to the product. By using the ABC system, activities can be classified as value-added and non-value-added activities. In order to improve the performance of the system, non-value-added can be eliminated.Despite the advantages of providing accurate costs, it requires additional effort and expense in obtaining the information needed for the analysis. However, a proper design tool can help to reduce time used for modeling and overcome the difficulties present in designing a cost model.The primary objective of this paper is to develop an ABC system for a sanitary-ware company and to compare the results of ABC with traditional costing methods. In other words, the aim of ABC analysis is to guide improvement efforts of management in the right direction by providing accurate information about activities.The organization of the paper is as follows: In section 2, the methodology of ABC is explained. A case study is presented in section 3 to illustrate the application of ABC in a company. Finally, in section 4, the conclusions and the future research directions are given. Some suggestions are offered to improve the performance of the company.2 Activity-Based Costing (ABC)ABC is an economic model that identifies the cost pools or activity centers in an organization and assigns costs to cost drivers based on the number of each activity used. Since the cost drivers are related to the activities, they occur on several levels:(1)Unit level drivers which assume the increase of the inputs for every unit that is being produced.(2)Batch level drivers which assume the variation of the inputs for every batch that is being produced.(3)Product level drivers which assume the necessity of the inputs to support the production of each different type of product.(4)Facility level drivers are the drivers which are related to t he facility’s manufacturing process. Users of the ABC system will need to identify the activities which generate cost and then match the activities to the level bases used to assign costs to the products.While using the ABC system, the activities which generate cost must be determined and then should be matched to the level drivers used to assign costs to the products.The implementation of the ABC system has the following steps:(1)Identifying the activities such as engineering, machining.(2)Determining the activity costs.(3)Determining the cost drivers such as machining hours, number of setups and engineering hours.(4)Collecting the activity data.(5)Computing the product cost.3 Implementation of the ABC Method: A Case StudyThe implementation study presented here took place in one of the leading sanitary ware companies in Turkey [7]. It has a production capacity of 6.8 thousand tons. Like many sanitary ware manufacturers, the company includes some common processes. First stage of the processes is done in the bulk-preparement department which is in charge of preparing the essential quantities of bulk bearing. Recipes are prepared for each production run and according to these ingredient recipes, the bulks are prepared by the electronically controlled tanks. After the bulk is ready, it can be sent to two different departments, pressured and classical casting departments.In pressured casting department, the bulk is given shape by the pressured casting process. The process uses automated machines and has shorter cycle times when compared to classical casting department. However, the bulk used in this department must have the characteristics of strength and endurance. The output of this department is sent to glazing department.Classical casting is the second alternative to produce sanitary ware products. In this department, most of the operations are performed by direct labor. The cycle times of the products are longer than the pressured casting department. The output of this department is shaped and casted bulk and sent to the glazing department, too.In glazing department, shaped bulk is glazed. This stage can be defined as polishing the products with a protective material from external effects. The output of this department is sent to tunnel oven.In tunnel oven, the products are heated over 1200 degrees Celsius. After staying in theses ovens for a period of time, the products are inspected by the workers. However, some of the output may have some undesired characteristics like the scratches, etc. In this case, these products are sent to the second heat treatment where they are reworked and heated again. The proper output is sent to packaging while the defected ones are sent to waste. Finally, in packaging department, products are packaged and shrunken.Company has been using a process costing logic for obtaining the proper costing of its products. Process costing is also a widely used costing tool for many companies. This method recognizes the following cost pools:Direct Labor: All workers taking place in the production are recognized as direct labor and this pool is the most common pool used in every stage.LPG-Electricity hot water: These items are important costing element in casting departments.Packaging: This cost is observed in the final stage of the firm called final packaging. It includes packaging and shrinking of the products.Overheads: This is also common cost pool for all the stages in the firm. It includes depreciation, rents, indirect labor, materials, and miscellaneous costs.In order to perform ABC calculations, process costing sheets are used. Because process costing aggregates the cost in the case of more than one product, it is difficult to obtain the correct results. The correct results with process costing can only be achieved when there is a single homogenous product. After analyzing the output of bulk preparement department, it is seen that bulk prepared for the two departments are the same which brings an opportunity for the analysis.Firstly, time sheets are prepared to learn how much of the labor time is used to perform the relevant activities. Workers filled the time sheet and as a result, the activity knowledge of the processes and related percentage times are obtained. The time sheets are edited and necessary corrections are made. While some of the activities are merged, some of them are discarded. After this stage, the wage data is requested from the accounting department and labor cost of the activities are determined.If the amount of the activities that each product consumes can be learnt, the product costing can be calculated by taking the sum of the costs of the activities consumed by these products. Observations and necessary examinations are done to reach this knowledge and the conversion costs are loaded onto the activities. Cost ofrent is loaded according to the space required for each activity and similarly, the power, depreciation and other conversion costs are loaded on the activities according to the activities’ consumption of the resources.After finding the product costs of the firm, the costs obtained by process costing methodology and the ABC results of the product costs are compared. From the results, it is seen that there are significant differences between some of the product costs obtained by the two methods.4 ConclusionsABC utilizes the activity concept and by using the activities, ABC can successfully link the product costs to production knowledge. How a product is produced, how much time is needed to perform an activity and finally how much money is absorbed by performing this task are answered by the help of ABC studies.From the ABC analysis, it is seen that while some of the products are undercosted, and overcosted, some of them give nearly the same results.In the analysis, the cost calculations of the bulk preparement department are performed using traditional costing method. When the outputs of the processes are identical or nearly identical, then ABC must be avoided to implement. Because ABC consumes lots of time, data and efforts, implementation of it has also a cost. For identical outputs, both ABC and traditional give the same results, so it is not logical to implement ABC.By the help of this analysis, product-pricing decisions gain importance. Pricing decisions can be done under the scope of these hidden losses and profits. According to the ABC results, the company will probably increase or decrease some of its product costs to gain more competitive advantage.The costing process of the company highlighted some weaknesses of the information system, too. These problems are also expected to be fixed in the future.As it is seen in this application, ABC is capable of monitoring the hidden losses and profits of the traditional costing methods. The existence of S-Curve shows which ones of the products are under or overcosted. As a further work, in the company, performance analyses are expected to be done and especially Balanced Score Card (BSC) implementations can be performed. The existence of the ABC database is an advantage for BSC applications since its financial phase recommends an ABC implementation. Kaizen applications and BSC can give the firm great advantages in the short and long run under the scope of ABC.The studies in literature promote that ABC is a promising method to support。